This quarter's ~$30B surge accelerates us toward the $500B milestone we predicted, while hyperscalers call it "still early."

The Big Three Side-by-Side:

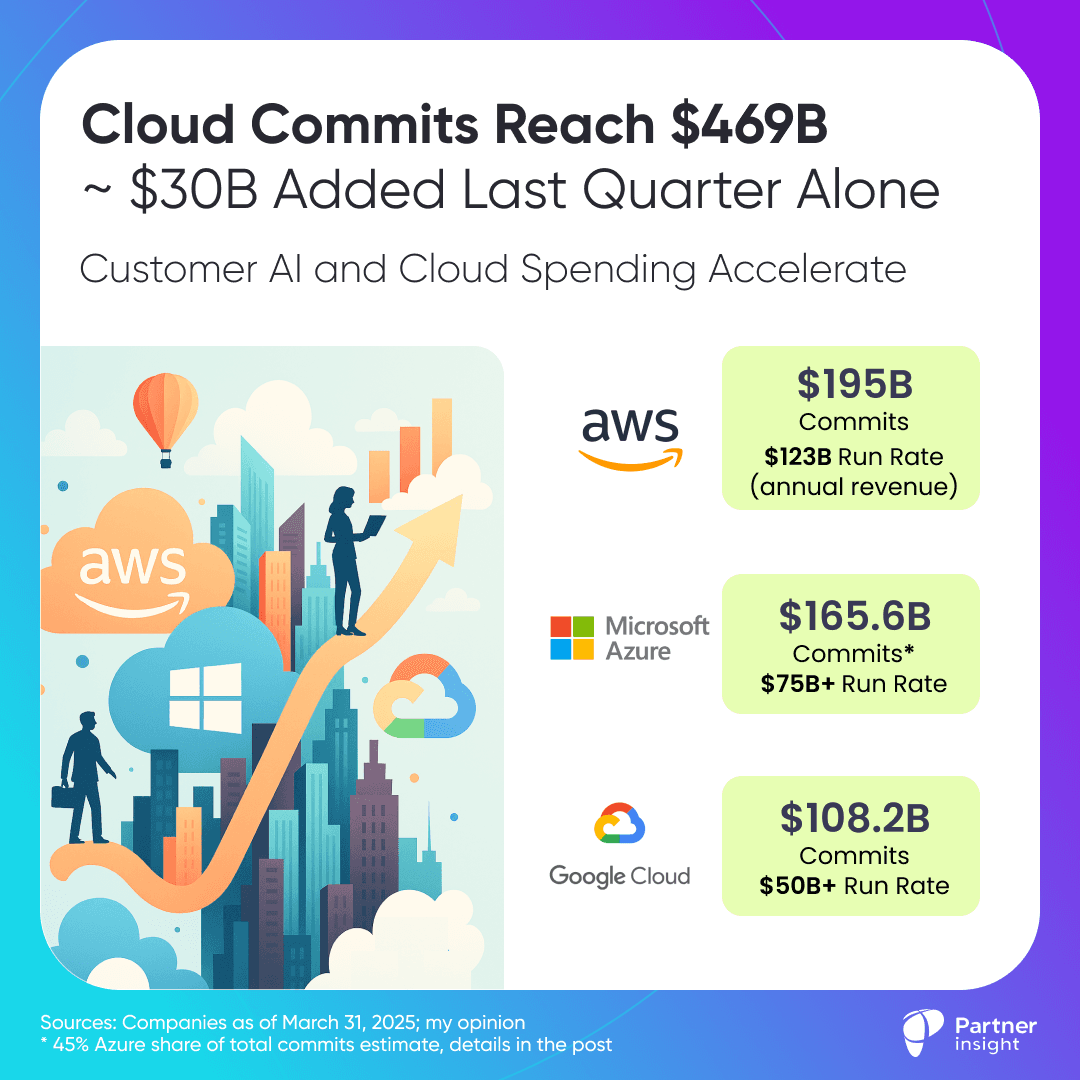

AWS

Commits: $195B (+$6B in Q2)

Annual Run Rate: $123B

Revenue Growth in Q2: 17.5% YoY

Notable: AWS Marketplace evolution into an AI distribution hub for agent discovery and deployment. Its recently launched "AI Agents and Tools" category features 800+ pre-built solutions from partners like Anthropic, IBM, and Salesforce.

Microsoft Azure

Commits: $165.6B (up $20B+ from last quarter**).

Annual Run Rate: $75B+

Revenue Growth: 39% YoY

**NB: I revised Azure share to 45% of Microsoft total backlog, based on CEO Satya Nadella's comments about Azure's run rate (and its share in Microsoft Cloud).

Notable: Microsoft's stunning 39% Azure growth and AI momentum. Microsoft processed "over 500 trillion tokens this year, up over 7x" through Azure AI Foundry APIs – what Nadella called "a good indicator of true platform diffusion beyond a few head apps."

Google Cloud

Commits: $108.2B (+$15.8B in Q2)

Annual Run Rate: $50B+

Revenue Growth: 32% YoY

Notable:

Gemini usage grew 35x YoY across 85,000+ enterprises showing adoption of AI workflows. "Over 1 million subscriptions have been booked for AgentSpace ahead of its general availability," Sundar Pichai emphasized.

AgentSpace interest highlights the appetite for AI agent usage. AgentSpace is GCP’s platform for AI agents, chat, and search. Its Agent Gallery has integration into Google Cloud Marketplace, pulling in partner-developed agents for seamless deployment.

Accelerating Ecosystems & Infrastructure Arms Race

Combined annual run rate approaches $250B with backlog representing nearly 2 years of future revenue—exactly our predicted trajectory toward half a trillion commits by end-2025.

Hyperscalers are building at unprecedented scale to capture AI demand. Amazon poured $31.4B last quarter, while still being supply-constrained. Microsoft guided next quarter to "over $30 billion" and Google upped FY2025 CapEx to ~$85B.

This infrastructure buildout will directly accelerate these ecosystems and their partner opportunities. More capacity means more customers, better performance, and expanded marketplace and co-sell opportunities for third-party solutions.

Key Alliance Imperatives:

Marketplace strategy becomes critical: With $469B in committed spend, your marketplace strategy determines access to this massive pool.

Partner ecosystem focus: Hyperscalers are investing heavily in partners to capture AI demand and maximize ecosystem value.

As hyperscalers are growing faster than ever and partners becoming critical to ecosystem success, how are you positioning for this half-trillion-dollar opportunity?

Now, let’s break down growth and key insights from each hyperscaler. As we covered GCP last week here (note that I slightly updated GCP commits number in the current post), I’ll focus on Azure and AWS below.

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value