AvePoint builds data governance + protection software used by 28,604 customers across cloud platforms.

They hit $416.8M ARR (+27% YoY), with RPO at $508M (+36% YoY).

These are standout numbers, especially as market debates if AI will disrupt SaaS.

But the real story is how they sell.

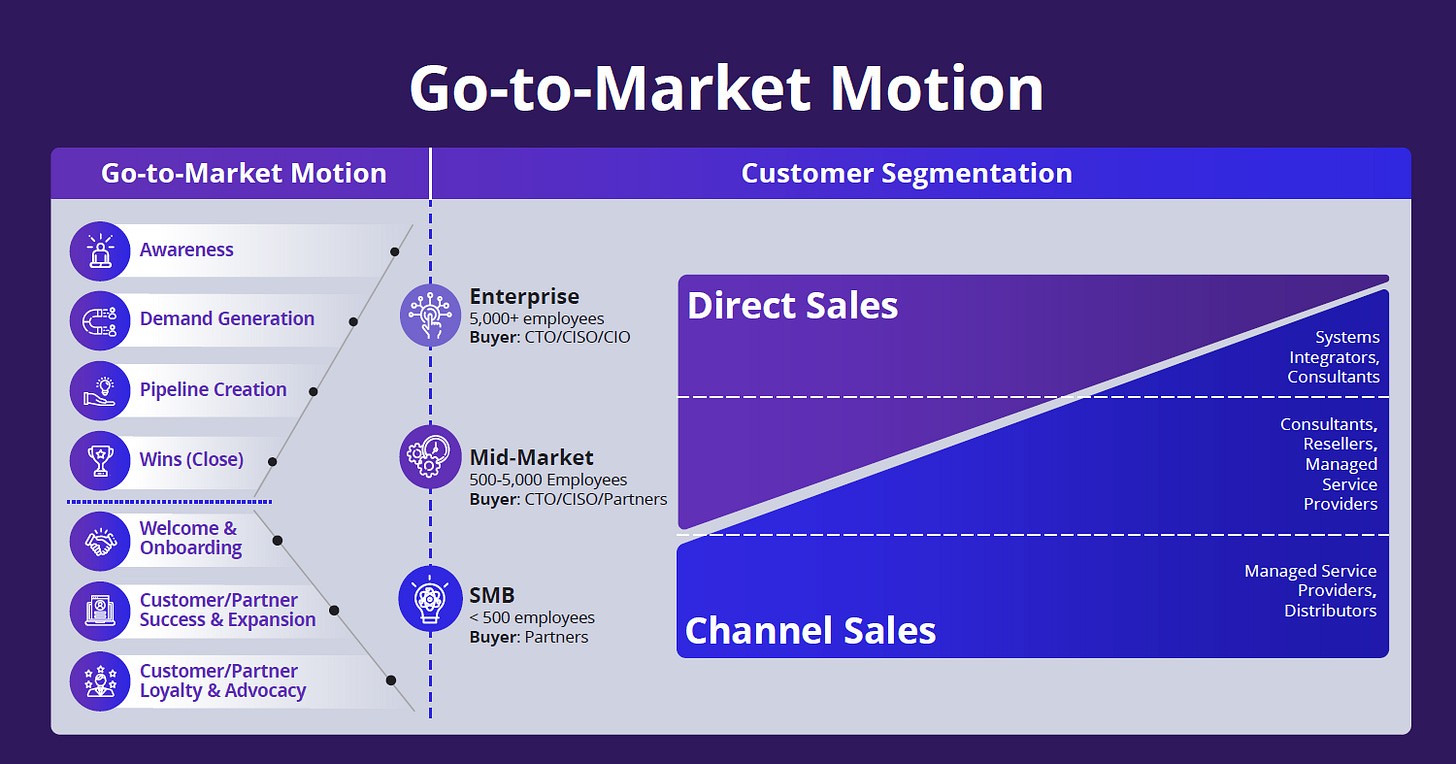

Their GTM breakdown

Enterprise (52% of ARR): primarily direct sales

Mid-market (28%): increasingly channel-led

SMB (20%): primarily through channel/MSPs

Channel growth in the last 3 years tells the story:

Channel ARR share: 47% (2022) → 57% (2025)

Channel partners: 3,403 → 5,859

MSP ARR: $19M → $62M (48% CAGR)

CEO Dr. Tianyi Jiang (TJ) last week:

“Our channel, focusing on MSPs, still our fastest-growing segment, unlocking SMB and mid-market. We have not seen slowdown in SMB, as some other vendors have seen.”

Channel isn’t just scale — it’s operating efficiency

Sales & marketing as % of revenue fell from 34.3% in FY24 to 31% in Q4 (and 32% for FY25).

AvePoint attributes this directly to scaling the channel strategy. They also hit Rule of 46 (ARR growth + operating margin), up from Rule of 31 two years ago.

Migration is the partner “tip of the spear”

AvePoint deliberately pushes services revenue to partners on migration projects, then retains the recurring software revenue on day-two governance, protection, and cost control.

Textbook land-and-expand through channel.

The hyperscaler GTM is expanding

AvePoint sells through Microsoft, Google Cloud, and AWS marketplaces, maintains strategic partnerships with all three clouds, and is moving beyond Microsoft 365 into multi-cloud workload governance across compute infrastructure.

They also signed a $340M five-year IT services consumption commitment (2026-2030) — a signal of how deeply embedded they are in hyperscaler economics.

AI doesn’t reduce their customer needs — it amplifies them

LLMs don’t eliminate security, backup, compliance, and policy control. They raise the stakes.

AvePoint is leaning into that with agent control / AI governance and pricing that mirrors hyperscaler economics: a blend of seat + consumption.

3 takeaways for alliance leaders:

Map partner strategy by customer segment. Clarity on “who sells to whom” prevents conflict and lets each motion scale.

Channel drives margin improvement, not just reach. Track S&M % of revenue as your channel matures — it’s the cleanest proof point for your CFO.

Treat hyperscalers as ecosystem opportunities for GTM: align marketplace procurement + co-sell + partner delivery into one motion

What’s your experience — does driving partners revenue accelerate customer adoption and stickiness?