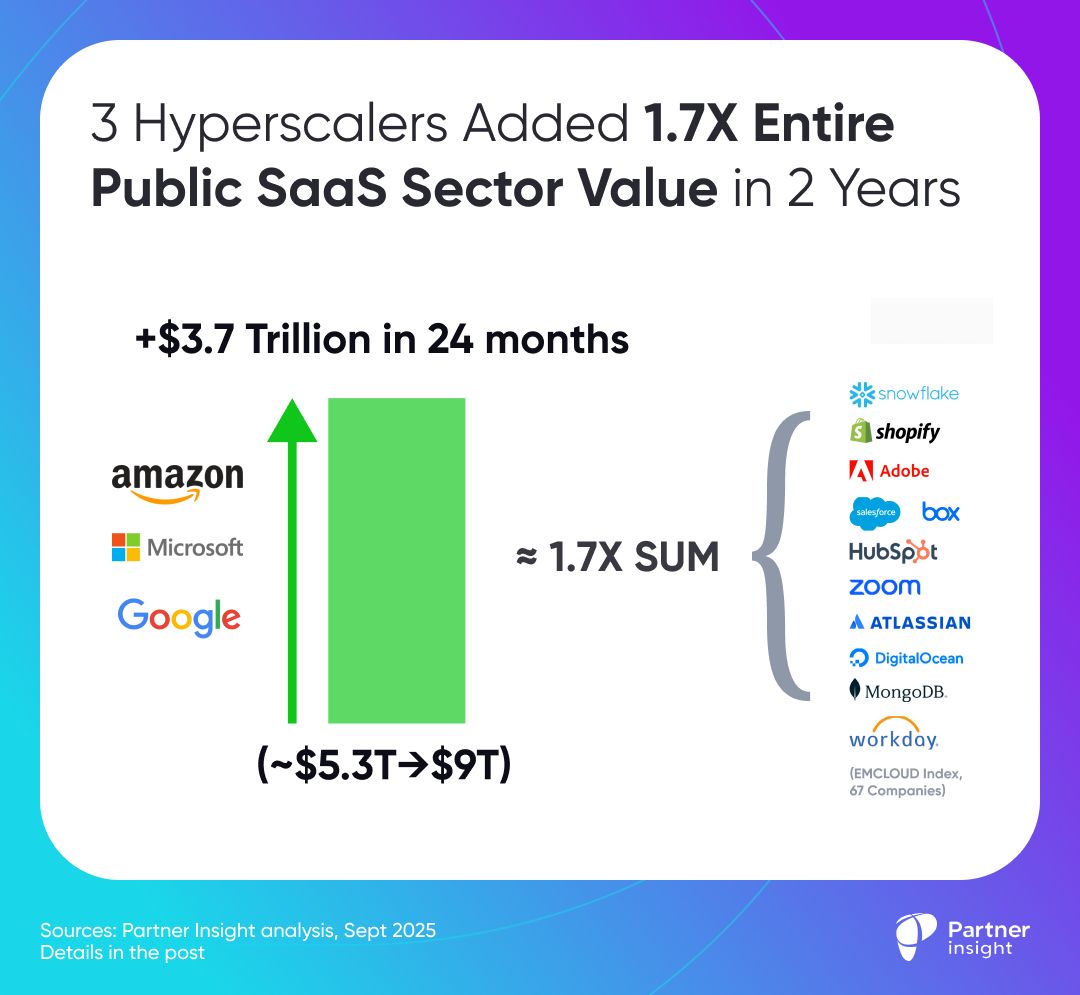

The 3 clouds (Microsoft, Amazon, Google) added ~$3.7T in market cap ~1.7X the value of the entire public SaaS sector

This shift marks a major change in the software world:

Value is concentrating around top cloud ecosystems that hold the keys to compute power, data, and now AI.

The rest of the software sector, built on top of these foundations, struggles to keep pace.

To see the divide, consider the BVP Nasdaq Emerging Cloud Index (EMCLOUD) as the cleanest proxy for the public SaaS sector.

It tracks 67 leading SaaS firms with over $500M in market cap, like Adobe, Salesforce, Shopify, Snowflake, and Workday, capturing the weighted performance of this entire group.

What changed (Sep ’23 → now):

⬆️ Big Three:

Amazon: $1.3T → $2.5T (+85%)

Microsoft: $2.3T → $3.8T (+62%)

Google: $1.77T → $2.84T (+60%)

Total: $5.43T → $9.09T (+67%, added $3.7T)

Hyperscalers: +$3.7T combined in the last 24 months. They also outgrew COVID peak valuations by 30-45%

➡️ EMCLOUD

The entire market cap of companies in Emerging Cloud Index is $2.2T.

Today the index at ~1,700; it grew just 15% from 2 years ago (~1,500).

It's still way below the COVID-era price peak of >3,000 at 2021.

The gap is still huge.

What the market is voting for with their dollars:

AI infrastructure at scale: Value accrues to the platforms that own compute, data, and distribution.

Ecosystems as strategy: Clouds compounded network effects across ISVs, services partners, and customers - faster than any single vendor could.

Marketplaces as the control plane for buying: A growing share of software spending routes through cloud marketplaces: consolidated billing, commit drawdown, fast procurement, and tighter integration.

So what? For software leaders & partners:

Align GTM and products with clouds: co-sell rigor, native integrations, and a packaging/pricing story that converts on marketplaces.

Partners win by solving the last mile: reference architectures, migration playbooks, security/compliance accelerators, and FinOps-ready deals.

Use marketplace to tap committed cloud spend and help buyers: Instrument the end-to-end: listing quality, private offers, field alignment, and post-sale consumption - not just top-of-funnel.

Zooming out

Clouds didn’t just help to build and host software anymore - they added an AI layer on top of their ecosystems and accelerated a powerful distribution layer underneath (marketplaces).

That twin engine explains the divergence: hyperscalers compound, while broad software is still re-rating to new buying patterns.

Exactly 2 years ago we launched our Cloud GTM Leader course

As these trends are accelerating, it equips alliance teams for this new reality.

We’re now at Cohort 12 (starts Sept 9), 250+ alumni, and countless stories of teams turning marketplace into revenue. If you’re doubling down on marketplace growth this half, join us.

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value