NVIDIA posted a record quarter: $81.6B in revenue, up 85% in a year, with $75B from the data center alone, up 92%. Demand, in Jensen Huang’s words, “has gone parabolic.”

But the more interesting number sits underneath.

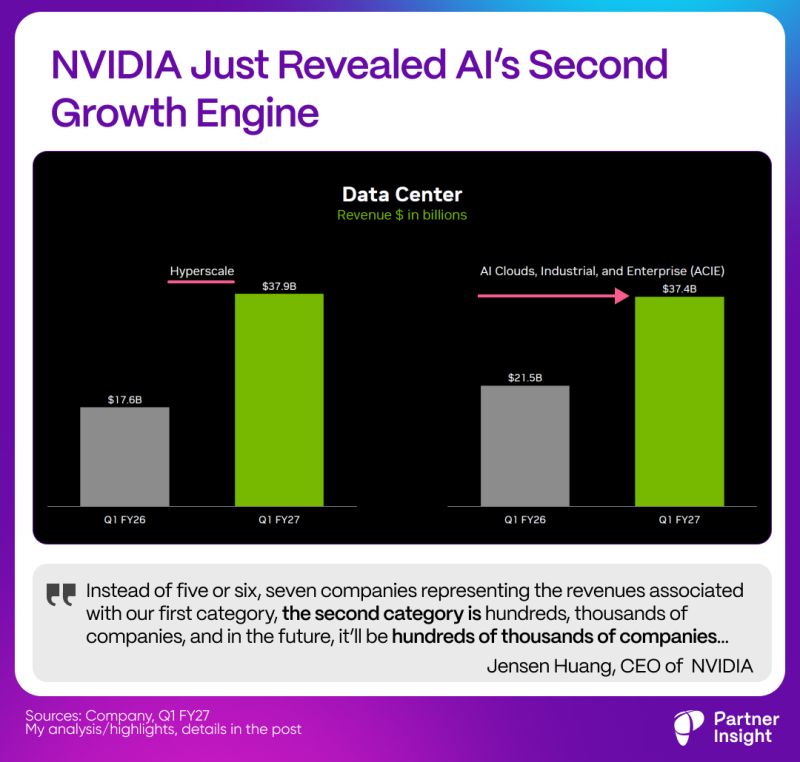

NVIDIA changed how it reports. Data Center now splits into two sub-markets:

Hyperscale — the public clouds (AWS, Azure, Google, Oracle) and the largest consumer internet companies

ACIE — AI Clouds, Industrial and Enterprise

NVIDIA only began reporting the business this way this quarter, so treat it as a fresh signal, not a long trend. Still, the two halves are now almost the same size:

Hyperscale: ~$38B, up 12% quarter on quarter.

ACIE: ~$37B, up 31% quarter on quarter.

Half of the data center business now sits outside the hyperscalers — and this quarter, that half grew more than twice as fast.

To be clear, the clouds are not slowing

They remain the largest route to market for NVIDIA.

As Jensen put it, hyperscaler capex is “a trillion dollars this year,” and “I have every expectation it’s going to grow from here.”

CFO Colette Kress added context:

“Analysts now forecasting hyperscale CapEx to exceed $1 trillion in 2027… AI infrastructure spending is on track to reach $3 to $4 trillion annually by the end of this decade.”

What changed is the scale of everything growing alongside big clouds.

So what is ACIE? NVIDIA defines it broadly — AI factories “across industries and countries.”

It didn’t give a full breakdown, but from what Jensen described on the call, it appears to span:

AI-native clouds (the neoclouds)

Enterprise AI factories

Industrial AI on the factory floor

Sovereign and regional clouds

On-prem AI builds

His framing: hyperscalers are 5 or 6 companies — a simple GTM motion for NVIDIA. This second group is “hundreds, thousands of companies. And in the future, hundreds of thousands.”

Frontier AI is now multi-cloud by default

That same diversification strategy is showing up at the frontier.

NVIDIA named Anthropic a new strategic partner, with Jensen noting it has “partnered with them to secure computing capacity across Azure, AWS, CoreWeave” — coverage that was “largely zero until just recently.”

No single cloud now owns the frontier model layer, except maybe GCP.

The signal is simple: AI is no longer scaling only on the big clouds.

It’s scaling across industries — into neoclouds, enterprises and factory floors.

Of course, NVIDIA has reason to tell this story. A more diversified buyer base means less dependence on a handful of clouds, and that’s a good narrative for its own stock.

But the direction is hard to argue with: AI is spreading — and the partners who reach these new buyers scale with it.

Where are you placing your bets this year?

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value