If you still think “marketplaces are for later, when we’re bigger” - this survey suggests the opposite.

KeyBanc Capital Markets + Sapphire Ventures recently published their 2025 SaaS Survey.

It’s especially relevant for alliance leaders because the median company is only $23.3M ARR, with respondents spanning < $10M to > $50M ARR.

These aren’t traditionally channel-heavy orgs… yet their go-to-market (GTM) center of gravity is shifting.

Here’s what stood out for me for marketplace + channel:

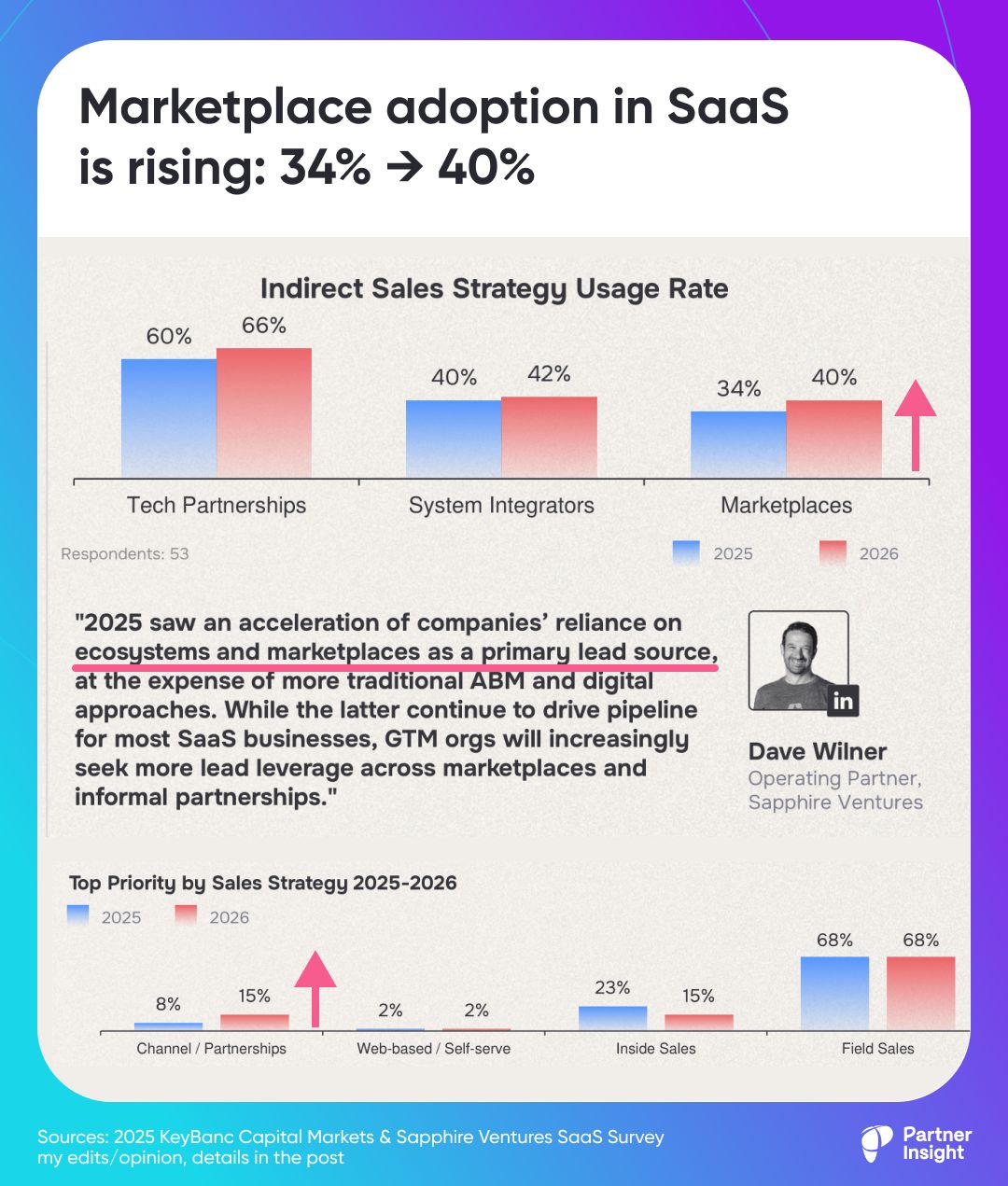

1️⃣ Ecosystems + marketplaces are becoming a primary lead lever

“2025 saw an acceleration of companies’ reliance on ecosystems and marketplaces as a primary lead source…” - underscored Dave Wilner, Operating Partner of Sapphire Ventures

2️⃣ Marketplace adoption is rising as an indirect sales strategy

Marketplace adoption: 34% (2025) → 40% (2026)

Tech partnerships: 60% → 66%

SIs: 40% → 42%

Marketplaces are already used by over a third of companies surveyed — and they’re growing fast, catching up with other ecosystem channels.

3️⃣ Channel is still “small” in ARR… which is why the trend matters

New ARR mix — how companies get revenue:

Field sales: 56%

Inside sales: 28%

Channel/Partnerships: 11%

Web/self-serve: 3%

The report highlights a shift toward channel/partnerships in 2025/26 at the expense of inside sales.

4️⃣ Companies want ecosystem leverage without building huge teams

Channel/Partnership Managers are only 6% of sales headcount in this dataset.

Practically, this means ~1 person below $10M ARR, 2 below $50M, and 3 at ~$50M.

If your partner team feels understaffed, you’re not alone.

Businesses expect advantage to come not from “more partner managers,” but from tighter partner + marketplace leverage.

5️⃣ Net-new economics are getting brutal

New-only CAC payback hit 37 months in 2024 (up from 31 months in 2022).

That’s why higher-intent routes (marketplaces, co-sell, partner referrals) are now critical — they can compress payback by tapping existing budgets + trusted paths.

6️⃣ AI is accelerating pricing complexity (and marketplaces benefit)

~50% of respondents are AI-native or AI-enabled. The rest are AI-interested.

Among AI-native/enabled respondents: 67% monetize AI; strategies split 58% subscription / 25% hybrid / 17% usage-based.

As pricing gets more complex, marketplaces + partners get more strategic because packaging and procurement become part of “the product.”

💡 For alliance leaders:

Marketplaces are becoming a distribution + customer acquisition engine earlier in the company lifecycle - exactly when teams are lean and efficiency pressure is high.

Curious: Is your 2026 plan built around scaling this channel?

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value