ICONIQ's State of GTM 2025 data (from GTM executives of 200+ B2B SaaS companies) shows channel partners as the key growth engine for companies that scale.

Note: ICONIQ uses “channel / partnerships” broadly, usually including SIs, resellers, cloud marketplaces, etc.

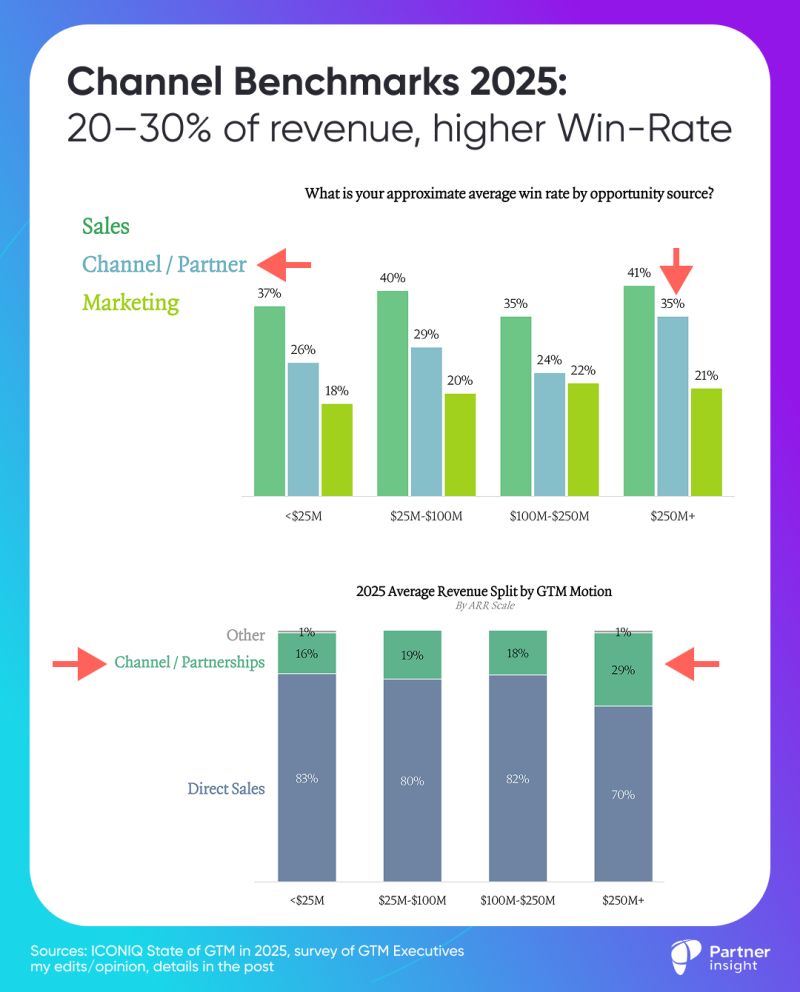

My key highlights:

Channel-sourced deals convert significantly better (~25–35% ) vs Marketing-led motions (18–22%)

Direct sales still wins at ~35–40% conversion, but the gap between Sales and Channel is far narrower in the mature stages, when companies truly lean into partnerships.

By $250M+ ARR, channel close rates approach direct-sales close rates (Channel ~35% vs. Sales ~41%).

Mature orgs usually operationalize partner motions—enablement, rules of engagement, shared pipeline, and seller incentives aligned to co-sell.

Channels contribute ~20% of revenue on average, rising to ~30% for $250M+ ARR companies

High-growth companies lean harder on partners: 25-30% channel share in recent years vs ~20% for slower-growth peers.

Below $25M ARR, channel share is lower at 16%—partnerships take time to build.

Above $25M ARR, 4 out of 5 companies generate ≥10% via channel (share rising with scale).

Infrastructure vendors rely even more on partners—30%+ channel share across stages. If you’re infra-adjacent, raise your channel ambition.

Software market is much tougher now

Sales cycles are longer

Average sales cycles stretched by +3–4 weeks YoY; (in fintech they jumped 12 weeks in the last 2 years)

Cost per opportunity is up significantly

It nearly doubled to 10K for <$25M ARR and increased across other categories, except for >250M (where channel is 29% of revenue, possibly giving operating leverage).

But consistent YoY reliance on channels is a key GTM lever, even amid AI disruptions

Despite shifts in AI-native vs. non-AI GTM strategies, channels remain stable at ~20% revenue contribution, signaling to alliance leaders that partnerships are resilient and essential.

3 Insights for alliance leaders

Start building channel/partnerships early (ideally before $25M ARR) for long-term scalability. If you wait to “get serious” at $100M+, you’ll pay a maturity tax later.

Treat channel as a core engine, not a side bet. It drives reliable conversions in complex buys and uncertain markets.

Benchmark your channel programs and accelerate partner enablement to capture this proven revenue stream.

Opportunity costs rose sharply for businesses below $250M, while those with mature channels maintained efficiency. As direct sales gets pricier, channels could be your oxygen.

Source: research

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value