BCG’s latest IT Spending Pulse shows the shift that is actually happening behind the catchy headlines dominating media.

Here are 7 signals that stood out for me:

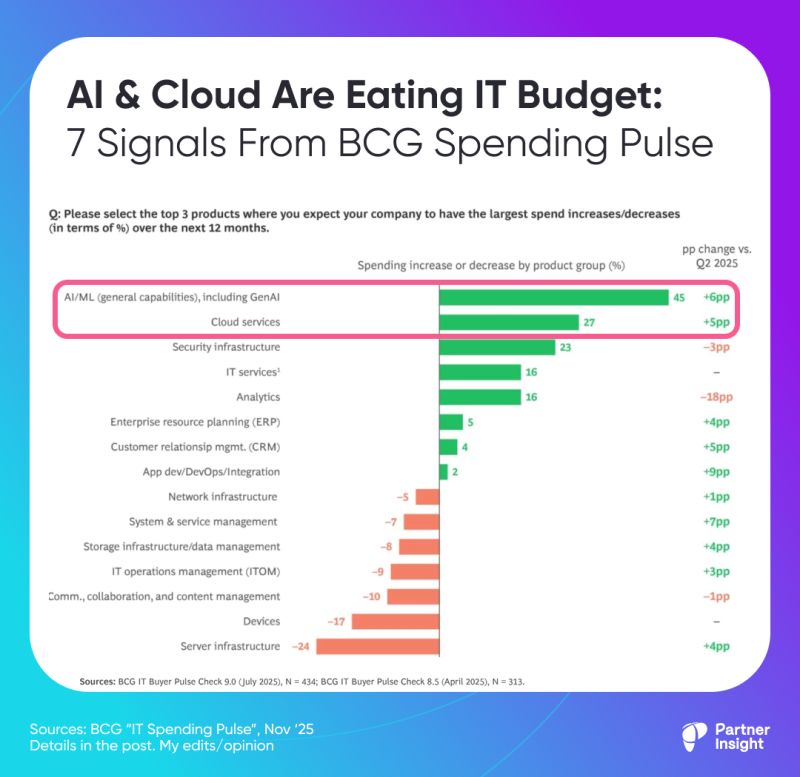

1️⃣ AI and cloud are growing in lockstep

AI/ML is the top net expansion area, with 45% of buyers planning to increase AI/ML spend

Cloud services are number 2 at 27%

Both are up strongly vs the last pulse (+6pp for AI/ML, +5pp for cloud), while devices, servers, and standalone analytics are flat or shrinking.

AI growth is coming with cloud growth, not instead of it.

Security is closely following cloud.

2️⃣ Digital transformation, growth and security are back on top

Cost-cutting is fading. CIOs now name digital transformation, growth, and security as their top three priorities.

As AI begins to prove its value; they modernize the core to grow it.

“Budgets are stabilizing and buyers are returning to strategic initiatives with renewed confidence” (BCG)

3️⃣ Budgets are rising again – with a maturity gap

IT leaders expect to grow spend by 2.9% in 2025 and 3.6% in 2026. This is cautious optimism, not a return to blank-cheque projects

More mature organizations dedicate 4.1% more revenue to IT vs less mature peers and expect 2X the ROI from GenAI and AI agents.

4️⃣ AI is delivering real – and measured – ROI

Current GenAI deployments show ~11% ROI, with expectations to rise to ~14% over the next 3 years (14.7% for AI agents).

Average ROI has moved slightly up from 10.6% at the end of 2024, pointing to a real growth rather than hype.

5️⃣ From “AI everywhere” to 3-5 winning use cases

Leaders are cutting the number of AI initiatives and concentrating on 3-5 use cases that work for them, e.g. analytics, customer service, marketing.

Fewer experiments, more tuning and scaling.

6️⃣ Platforms and specialists beat “do-everything” providers

“Satisfaction with technology providers varies sharply” (BCG).

8 out of 10 buyers are satisfied with digital platforms - most satisfied group

SaaS and specialist services sit around 63%.

It drops to 48% for MSPs - clearly buyers prefer focused experts.

7️⃣ Supplier consolidation is accelerating

“Supplier consolidation reflects a pragmatic push to simplify portfolios, fund innovation, and reduce risk.”(BCG).

Even in security, where spending remains robust, “buyers are consolidating vendors as they seek fewer but stronger tools to ensure resilience and manage complexity.”

Why this matters for alliance & marketplace leaders

Treat AI, cloud, and security as one conversation, find a way to join it

Align your product in marketplaces as the easiest path to (enable) scale pragmatic AI programs on top of trusted clouds

Lean into consolidation: be the focused, high-ROI specialist on your hyperscaler’s platform, and surround yourself with a curated list of high-caliber partners (not a long tail of noise)

Source: BCG

P.S. If you found these insights valuable, please forward it to your alliance lead or cloud/GTM counterpart - it’s how this community shares what works.

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value