The Rise of AI Agents

Unlike traditional apps with defined workflows, coming AI agents will make decisions, and take autonomous actions. This shift is profound - we're moving from apps that follow rules to agents that understand context and reason about business processes.

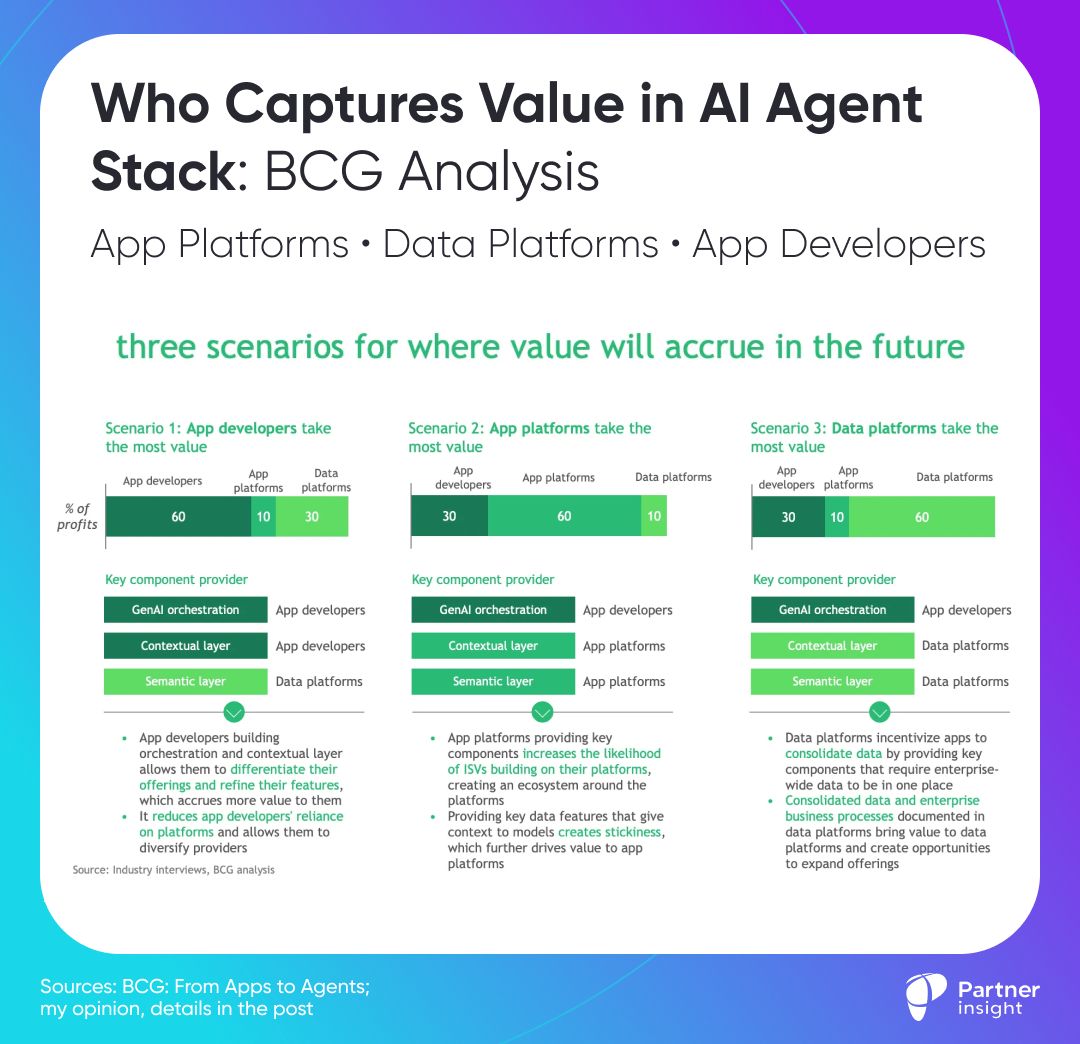

In this new agentic era, Boston Consulting Group (BCG)'s analysis reveals 3 key players could each capture major value, but with different strengths:

👩🏻💻 App Developers

Examples: Ema, Glean

Emerge with the highest probability to win, expected to capture 30-60% of value in any scenario.

Why? They own the critical GenAI orchestration layer that manages AI models, optimizes performance, and handles complex reasoning.

This can't be easily commoditized because it requires deep use-case understanding and continuous innovation.

🗃️ Data Platforms

Examples: Snowflake, Databricks

Data Platforms show remarkable potential, capturing 30-60% of value in 2 out of 3 scenarios.

Their power comes from providing the foundation for AI applications: enterprise-wide data integration, semantic understanding, and contextual intelligence. As AI apps become more sophisticated, this foundation becomes increasingly critical.

But here's where it gets interesting:

📊 App Platforms:

Salesforce, SAP

They face a stark contrast. In 2 out of 3 scenarios by BCG, they're getting just 10% of value.

But there's one scenario where they capture 60% - the highest potential share. What drives this dramatic difference?

The winning scenario for App Platforms hinges on their unique advantages:

Control of domain-specific data and business logic

Ability to create sticky solutions by embedding AI directly into existing workflows

Power to build ecosystems around their platforms

But BCG missed another category of players reshaping the game entirely:

☁︎ Cloud Hyperscalers with their marketplaces

Their position is more nuanced and powerful than it might appear at first glance.

They span all three categories:

As Infrastructure Providers

Offer essential AI/ML services

Power the compute needed for AI workloads.

As App Platforms:

Run powerful cloud marketplaces, with growing ecosystems of B2B apps and services

Enable deep integration across services

As Data Platforms:

Provide enterprise-scale data infrastructure

Offer advanced AI/ML tooling

Enable cross-service data integration

This triple position gives them unique advantages.

While app developers, data platforms, and app platforms fight for dominance in their respective layers, clouds are in a prime position to win regardless of which scenario plays out.

They're building the entire ecosystem that everyone else will operate within.

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value