ServiceNow: one SI drives 11% of revenue; they have $4.7B in cloud commitments, while hyperscaler adoption is shifting their business mix.

ServiceNow still growing >20% at $15B+ scale — in a market that’s questioning whether non-native AI software can grow at all.

They just reported a better-than-expected Q4, 21% subscription revenue growth, and RPO up 25% (21% in CC). That’s a demand signal, not a narrative.

Here are the partnership lessons hiding in plain sight:

1️⃣ Partners are core to their revenue

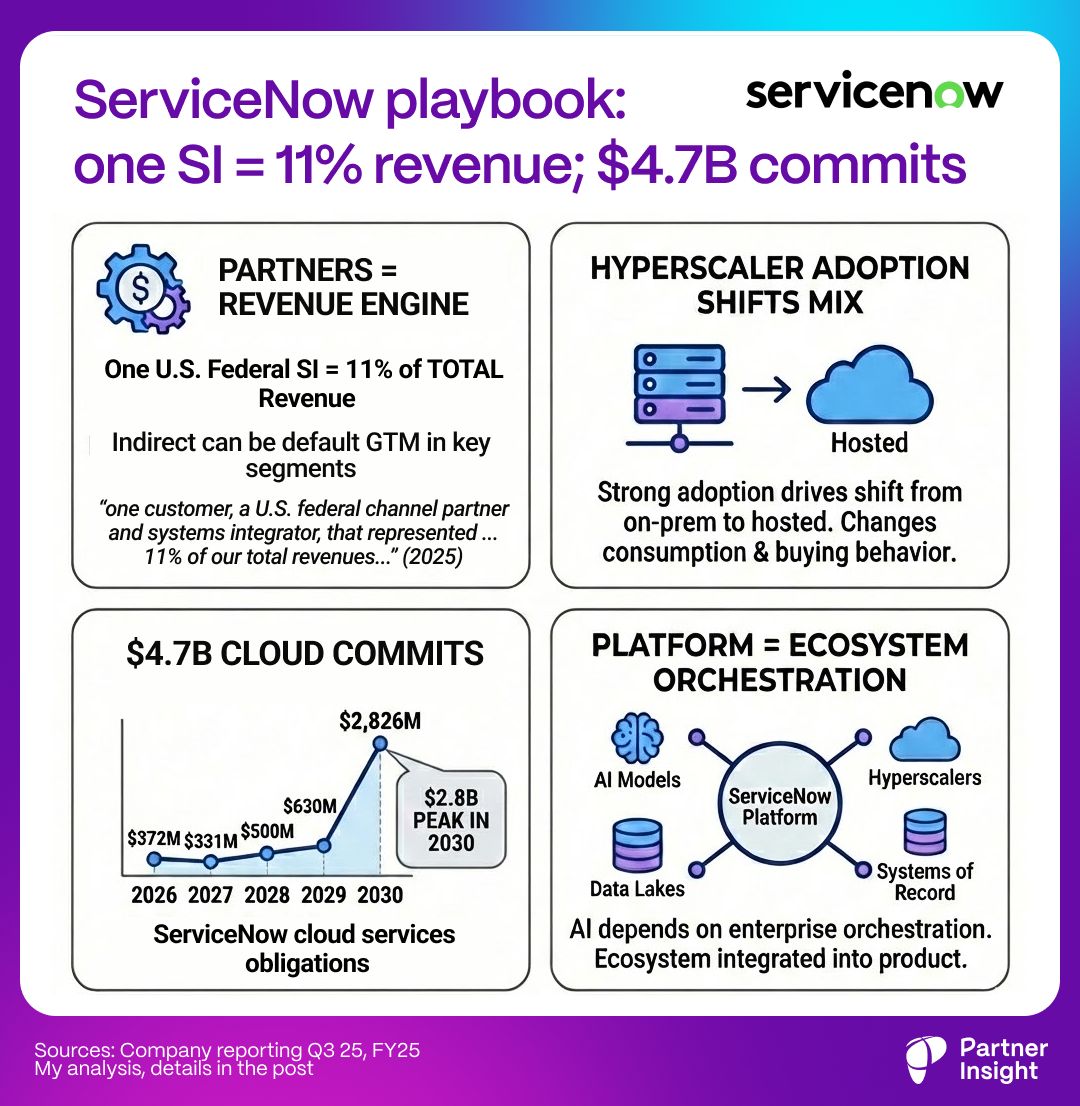

ServiceNow discloses that an “increasing portion of revenue flows through partners”.

That’s a shift many companies talk about, but few admit in black-and-white.

2️⃣ Some segments are structurally indirect (& concentrated)

They explain that a substantial majority of U.S. government sales are indirect via distributors, resellers, and service provider partners.

One U.S. federal channel partner / systems integrator represented 11% of total revenue.

This is the part alliance teams often underestimate: in some segments, the partner isn’t just helping close deals - the partner is the buyer-facing GTM default.

3️⃣ Hyperscaler adoption is so strong, it changes business mix

They specifically called out a mix shift from on-prem to hosted that was “partially driven by strong adoption of hyperscaler offerings.”

That reframes hyperscaler GTM as more than distribution: It changes how customers buy and consume your platform.

4️⃣ ServiceNow itself is living in the “commit economy”

ServiceNow disclosed $4.7B in non-cancellable cloud services obligations — and $2.8B of that sits in 2030.

Even at $15B+ scale, ServiceNow isn’t just selling through hyperscalers — they’re also a massive, long-dated buyer in the same commit economy.

And the spike in 2030 shows how multi-year cloud commitments concentrate.

5️⃣ Their “platform pitch” is really an ecosystem pitch

CEO Bill McDermott: “AI doesn’t replace enterprise orchestration. It depends on it.”

AI isn’t eating the enterprise platform. It’s eating “feature” vendors.

Real value happens when models are built into workflows where real decisions are made.

His definition of a modern platform is not “we have AI.” It’s: the platform has to work with language models, hyperscalers, data lakes, and systems of record — and stitch them into something coherent.

For alliance leaders, that’s a strong signal that the ecosystem is becoming part of the product.

Partnering with all the power centers at once

ServiceNow expanded partnerships they called out this quarter include Microsoft, OpenAI, Anthropic, NTT DATA — and they explicitly highlight relationships with Amazon Web Services, Google Cloud, Microsoft Azure, and NVIDIA.

Question for alliance leaders:

In your GTM, are partners and hyperscalers still ‘supporting’… or are they becoming the operating system for growth?

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value