ICONIQ, one of the largest VC/PE funds, surveyed 300 software execs - CEOs, revenue chiefs, and product leaders — for their AI report.

It highlights that “AI builders increasingly formalizing partner ecosystems”, leaning on partners and hyperscalers to drive revenue.

My takeaways:

Channel, partnerships and hyperscalers are driving revenue for AI companies

“Channel and partnerships are emerging as a meaningful growth lever, particularly with consulting firms, hyperscalers, and PE-backed platforms, contributing directly to pipeline generation and post-sale implementation.”

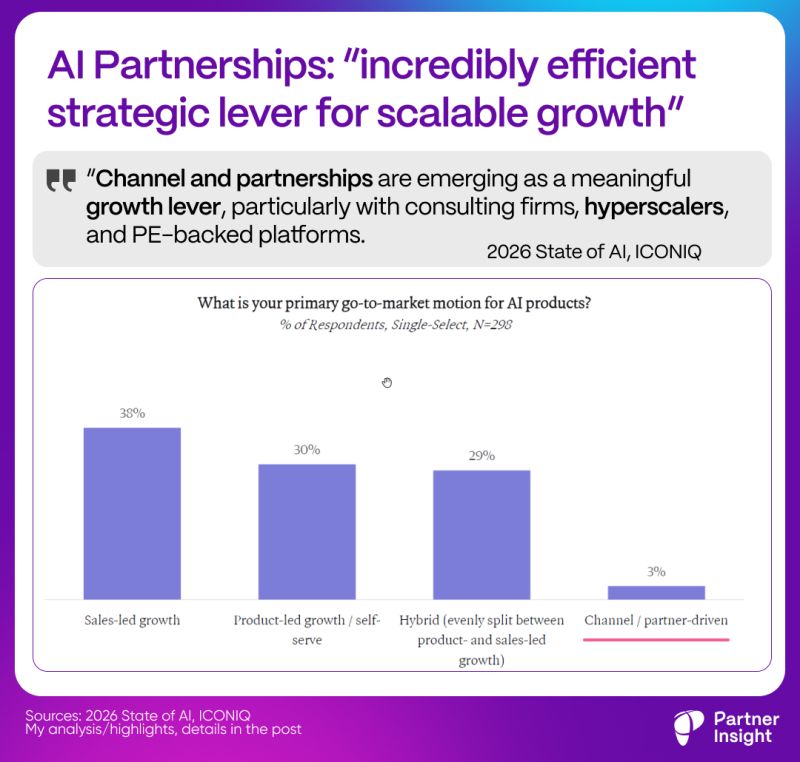

Primary GTM motion is still sales-led at 38%

product-led/self-serve is 30%

hybrid is 29%

and channel/partner-driven is 3%

What it means: Partnerships are not yet the main route to market (they rarely are), but they are an important force multiplier across sourcing, credibility, implementation, and expansion.

Partnerships need to be built earlier than most companies think

Rob Bernshteyn, former CEO of Coupa highlights the importance of timing:

“Partnerships are an incredibly efficient strategic lever for scalable growth. The earlier companies lay the foundation (ideally well before $25M ARR) the more likely they are to see channel revenue become a meaningful contributor down the line.”

Companies that wait until scale to build partner ecosystems may miss the compounding effect of partner-led revenue.

AI is forcing a rethink of GTM

“Go-to-market strategies for AI products are becoming more complex and diversified” — highlights the report

“While sales-led motions remain the most common, nearly 60% of companies now employ hybrid or product-led elements, reflecting the need to combine enterprise selling with hands-on product experience.”

The self-serve-plus-sales motion is now the norm — it maps on how cloud marketplaces operate with free trials and PAYG layered onto an enterprise sales process.

AI stack is going multi-model, multi-cloud

Companies now use ~3.1 model providers on average, up from ~2.8 six months ago.

Orchestration is beating allegiance to a single vendor in AI — the same logic we see in multi-cloud.

Two insights for alliance leaders:

3% shows that partnerships doesn’t have to be your primary motion to become one of the largest revenue drivers.

Leaning on partnerships and cloud GTM is an early-stage decision. Partner infrastructure built before $25M ARR compounds. Bolted on at $100M, it is harder to catch up because GTM motion, and sales habits are already set.

Source: research.

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value