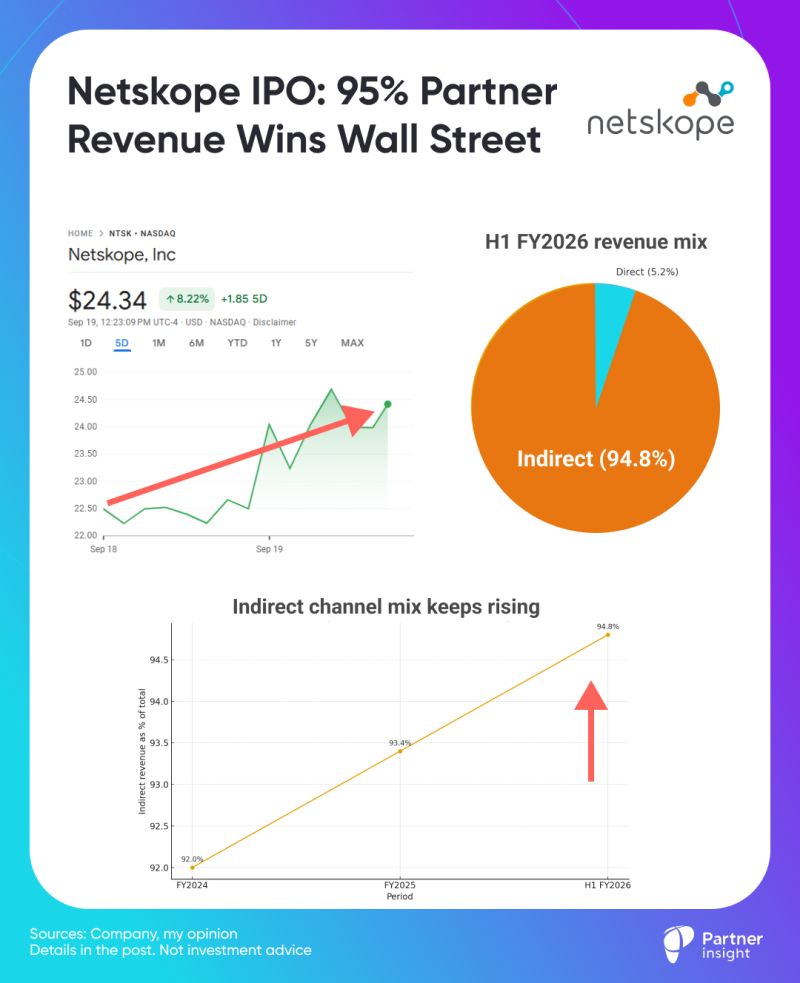

If a 94.8% indirect revenue mix sounds extreme, look at the tape: Netskope is trading >25% above its IPO price last week.

Oversubscribed IPO creating awareness flywheel

Netskope raised $908M, valuing it at ~$9B with the book reportedly ~20X oversubscribed.

CEO Sanjay Beri positioned IPO as marketing amplifier rather than need to fundraise: "The big reason why we would go public is not for capital... It's for awareness". Smart strategy.

Partner-first: 95% of revenue is indirect

Partner contribution climbed from ~92% in 2024 to 94.8% in H1 FY26—meaning the channel drives virtually all growth at Netskope.

ARR hit $707M (growing +33% YoY) as of Jul 31, 2025.

Top-5 partners drive 33% of company revenue, supporting a "sell-through partners, co-sell on big deals" GTM thesis. But it's also about scale, not just hero deals.

Scale of the partner ecosystem

Netskope works with 1,600 channel partners worldwide across VARs, MSPs, distributors, GSIs, and MSSPs. (CRN)

Top five drive 33% of total revenue—a concentrated bet on key relationships. So enablement and joint execution with a focused core really matter.

The largest single partner represents 13% of sales, creating both efficiency and dependency risk.

Geographically, international partners are delivering:

EMEA revenue surged 48% to represent 24% of total sales, while APAC contributes 19%.

In Asia-Pacific specifically, Netskope operates 100% through partners with zero direct sales—a pure channel model as international markets outpace domestic growth.

Marketplaces and hyperscalers are core to GTM

Netskope showed strong Amazon Web Services (AWS) Marketplace traction, doubling revenue QoQ as early as 3 years ago.

Ahead of the IPO, they added Netskope One DSPM to AWS Marketplace's new AI Agents & Tools category—smart focus on agentic AI and packaging for how buyers want to purchase now.

Netskope is also selling via Google Cloud Marketplace and integrated in broader Google ecosystem (Workspace Marketplace), plus integrations across Cloud WAN and Google SecOps.

Why the channel actually wins

SASE projects need POCs and implementation services - partners make it repeatable. Canalys noted ecosystems like Netskope's let partners create $2 in services per $1 of product, rising to $4-$6 on platform plays—exactly why channel-first models compound over time.

The company works with global distributors and GSIs (WWT, Exclusive Networks, Ingram Micro, Deloitte/TCS), MSSPs, cloud alliances, etc. That structure reaches Fortune/Global 2000 at scale, not just isolated logos.

Netskope becomes the second pure-play SASE firm publicly traded alongside Zscaler (March 2018 IPO).

Notably, Zscaler just reached $1B TCV in AWS Marketplace sales - validating the partner-first and Cloud GTM approach Netskope is pursuing.

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value