But what does this mean for partners?

Andreessen Horowitz put it plainly:

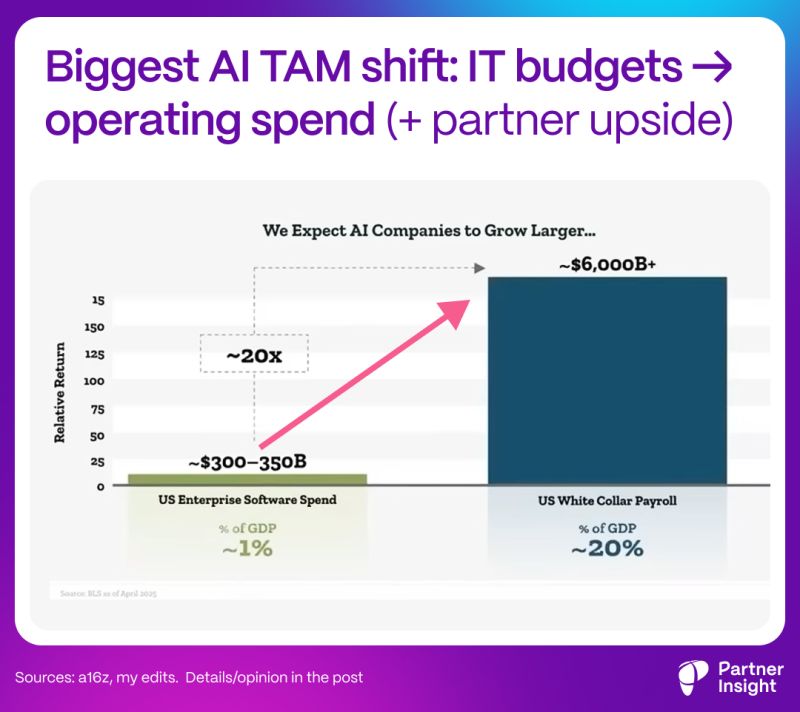

AI isn’t just expanding the SaaS market — it’s now benchmarked with a much larger spend pool: labor.

New TAM math is staggering:

Even if most AI value flows to customers (a16z rule of thumb is 90% of software-driven value goes to customers, 10% to vendors), 10% of a market that’s 20X larger is still enormous.

You’ve probably heard what makes this cycle different

AI adoption spreads >5X faster

Costs collapse as model capabilities ~2X every 7 months

Infrastructure buildout is being funded primarily by hyperscalers spending ~$400B annually on AI capex. They bear the burden — and, as a result, they also become the gravity wells for ecosystems where partners capture value.

Here’s the part that matters most:

New rules of software

1️⃣ Systems of action will matter more than systems of record

Software that only stores data becomes less compelling. The new moat is agentic capability layered on top of workflows — software that can do the work, not just track it.

As we move from systems of record to systems of action, the winners won’t be the ones that help store the truth — they’ll help execute it.

2️⃣ Defensibility becomes operational

Models will swap out via API. What doesn’t swap easily is everything around them: integrations, rules, approvals, security, governance, and trust. Stickiness shifts from UI to embedded process.

3️⃣ Pricing shifts from seats to outcomes

Seat-based pricing starts to break when software replaces tasks. The direction of travel is clear: buyers want to pay for value created, not the number of logins.

What this means for partners + Cloud GTM leaders

The partner ecosystem becomes the moat — because the bottleneck is change

Bottleneck isn’t an AI model choice. It’s org change: data readiness, workflow redesign, governance, security, and adoption.

Models are swapping out via API. What doesn’t swap easily is change management. That’s why partners become the moat.

Trust + access become GTM advantages

In an agentic world, “who can run in production” matters more than “who demos best.” Partners who can deliver safe rollout, controls, and proof become power brokers.

Marketplaces become the rails for outcome buying + governance

If significantly more software is built and used by more people, more often, companies will desperately need rails to evaluate, buy, govern, expand, and measure.

Marketplaces help to experiment safely and turn into repeatable purchase — with packaging, commits, and expansion built in.

They will be a governance layer for agentic software: approved vendor, billing, terms, and usage controls in one place.

Net:

Software market may feel threatened — but the bigger story is software moving into work, expanding the pie, and creating a new layer of value.

What’s your take?

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value