This signals investors now price in durable AI monetization across Search, Cloud and YouTube - while key headwinds ease.

The latest leg up followed:

a favorable U.S. ruling letting Google keep control over Chrome/Android

outsized Cloud and AI momentum

In many ways this $3T mark validates Alphabet's pivot from mostly dominant search engine to AI-cloud powerhouse.

But how much of this success is Google Cloud?

Where Google Cloud Stands Out

Growth Rate

Fastest among Alphabet businesses and one of the fastest among major global cloud providers.

AI Leadership

Google Cloud excels in AI and machine learning infrastructure, recently earning large deals and partnerships (e.g., with Salesforce and OpenAI) and leading generative AI integration for enterprises.

Most of the largest AI labs —including OpenAI and Anthropic—now use GCP.

Margin Improvement

Cloud’s operating profit more ~2X in a year due to scale and efficiency improvements, marking a shift from years of operating losses to sustained profitability.

Scale & growth (last Q2 numbers)

Google Cloud revenue hit $13.6B in last quarter Q2, growing +32% YoY,—reaccelerating from Q1's 28% and surpassing estimates.

Its annual run-rate is $50B+, driven by booming AI demand.

Cloud is now ~14% of Alphabet revenue.

Profit engine

Cloud operating income was $2.8B with 20.7% margin (up from 11.3% a year ago).

That margin expansion is the “profit flywheel” investors were waiting for.

Cloud is ~9.0% of Alphabet’s total operating income in the last quarter.

Backlog

GCP backlog (customer cloud commits) hit $106B, growing 38% YoY and 18% sequentially.

Commits jumped an incredible $15B+ in just the last quarter alone.

Essentially next 2 years of GCP revenue is already signed by customers.

Among the largest CapEX among hyperscalers

The $85B 2025 capex plan they announced is helping to cement their strong position in AI to serve training/inference demand.

Why the $3T milestone matters (ecosystem, ISVs, partners):

Google now has stability, capital and ecosystem for more aggressive investments in the fastest growing parts of its business - AI and cloud

Budget gravity as Alphabet is channeling record CapEx into AI + Cloud

More capacity, more regions, more GPUs/TPUs, more data centers = more room for ISVs riding AI-adjacent workloads

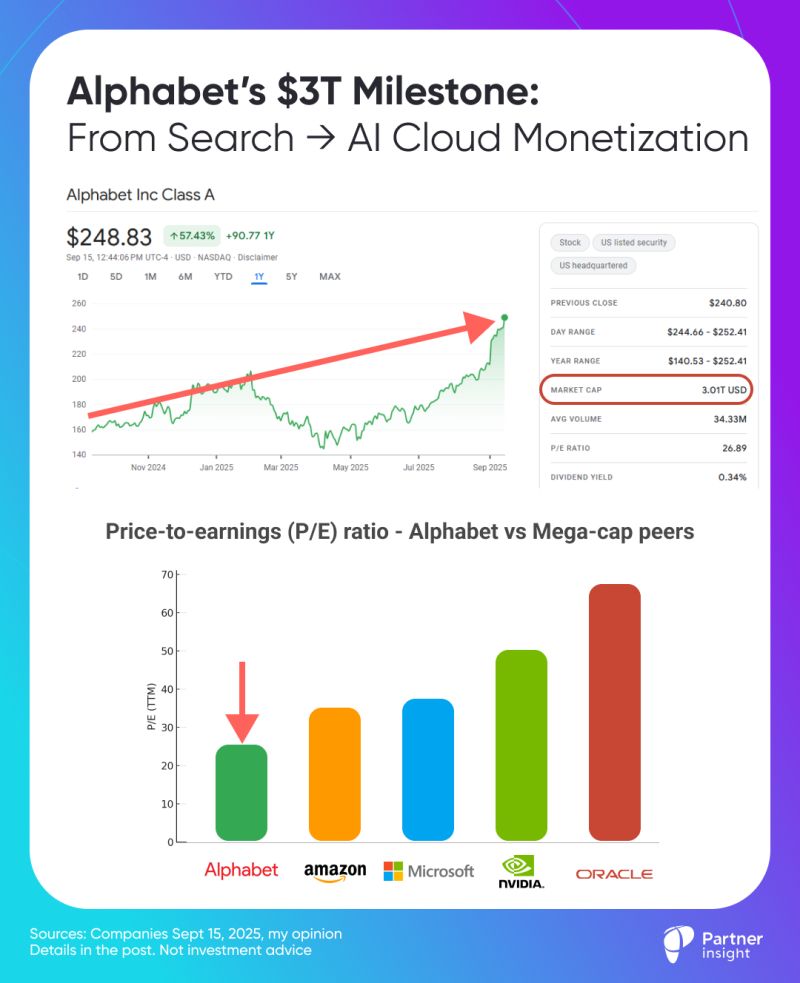

Even at $3T valuation, Alphabet trades at a significant P/E ratio discount to its mega cap peers.

This suggests there is still a lot of room for growth and AI acceleration.

Price-to-earnings ratio (P/E, Sept 15)

Google - 26

Amazon - 35

Microsoft - 38

NVIDIA - 50

Oracle - 68 (!!!)

What's your take on this growth story?

PS. Not investment advice

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value