3 hyperscalers will spend $255B+ on AI infrastructure this year, but every $1 in capex requires ~$4 in revenue to justify it. That means they’re modeling >$1T/year in incremental ecosystem revenue.

Bain’s recent analysis breaks down this trajectory: It estimates the world will need ~$500B/year of new data-center capex to meet AI compute demand by 2030. To make it sustainable, this would require $2T/year in revenue—a 1:4 capex-to-revenue ratio.

And 2025 hyperscaler capex is already pointed there.

AWS is projecting $100B+, Microsoft $80B, and Google $75B for 2025 alone. Commitments keep escalating.

Headlines also pointed to OpenAI–Oracle capex deals worth ~$300B.

Plus a NVIDIA-OpenAI $100B partnership tied to 10GW of AI systems - signals of how much revenue hyperscalers and chipmakers expect to pull through their stacks.

The list goes on….

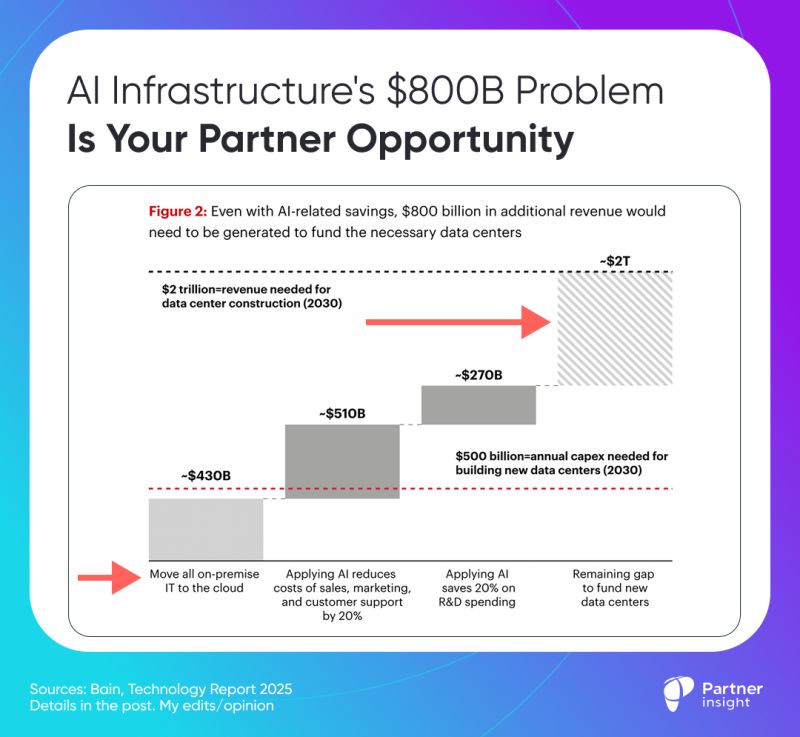

Revenue Reality Check

Even if enterprises:

move all on-prem IT to cloud (+$430B),

reinvest AI-enabled 20% savings in sales/marketing/support (+$510B),

and reinvest ~20% R&D savings (+$270B),

…there’s still an $800B annual gap to fund the build.

That’s Bain’s point: efficiency alone won’t pay for the new compute - new revenue streams must.

Where does that massive revenue shortfall come from?

One of the answers is Services. That is the next battleground where software gets rebuilt around AI agents to AI-enable jobs.

Services share of US GDP: ~72.3% (Q1’25, BEA)

The U.S. service economy alone is ~$24T annualized (Census), including:

Professional services ~$3T

Financial services ~$7.3T

Healthcare ~$4.3T

Information servicing ~$2.6T,

Admin/support ~$1.4T

I’m not saying AI replaces services; but many of these services will be increasingly AI-enabled or AI-delivered.

However, hyperscalers can’t capture this trillions in services economy transformation alone.

They need ISVs, SIs, and specialized partners to build AI-enabled solutions that convert traditional service delivery into cloud-consumed outcomes.

More good news - cheaper, more available services - higher the demand for them.

In fact, Microsoft’s research (Nov ‘24) argued that gen-AI could add $3.8T to the U.S. GDP by 2038, implying ecosystem-supported scenarios where AI’s revenue pull grows meaningfully beyond today’s models.

What this means for Alliance leaders

The math is clear: hyperscalers aren’t competing for just existing cloud budgets. They’re racing to capture revenue from AI-enabled service economy transformation.

The capex wave sets a revenue quota for ecosystems.

If your solution demonstrably pulls consumption and/or comes with services that compress time-to-value, the clouds need you to hit trillions of dollars of revenue they are implicitly committing while building this capacity.

If not, you’re maybe swimming against a very expensive AI tide.

Or underestimating the power of the ecosystems that are getting built.

Image: Research

P.S. If you found these insights valuable, please forward it to your alliance lead or cloud/GTM counterpart - it’s how this community shares what works.

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value