But if investors now reward capex that turns into revenue, hyperscalers will pressure-test every GTM motion.

Marketplace-first + co-sell to drive consumption and AI will become even more “core.”

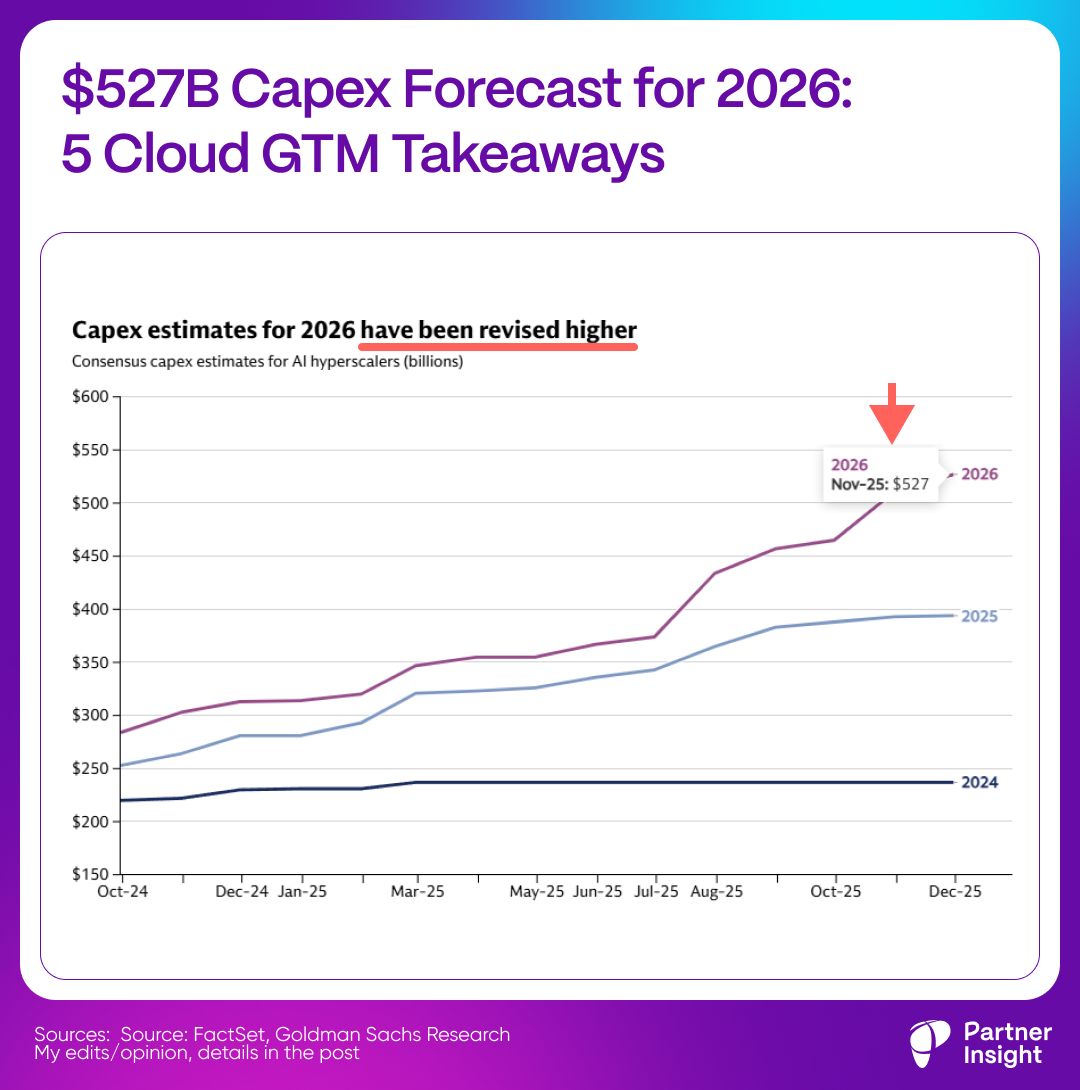

Consensus 2026 capex for the AI hyperscalers keeps rising. It’s now $527B (up from $465B at the start of Q3 earnings). And consensus has been underestimating spend for 2 years (20% implied growth; vs >50% actual).

For context: Amazon, Microsoft, Google and Oracle spent $105B+ in capex in calendar Q3 2025 alone.

Here are 5 implications for Cloud GTM leaders:

1️⃣ The constraint is not cash. It’s capacity + investor patience

The real constraints are “supply bottlenecks or investor appetite,” not cash flow / balance sheet capacity.

Alliance-leader translation:

Hyperscalers are still in “build mode,” and they’re not slowing because they can’t spend — they’ll slow only if they hit supply bottlenecks or if markets force discipline.

That’s a very different planning environment for partner GTM than a normal IT cycle.

2️⃣ When spend is this high, monetization becomes a core metric

Investors are now rewarding companies that show a clear link between capex and revenues.

So hyperscalers will push harder on the monetization:

marketplace-first deals

co-sell tied to consumption

attach plays that pull through GPU + data + platform usage

3️⃣ Hyperscalers are not moving as one

Average stock price correlation across AI hyperscalers fell from ~80% to ~20% since June — as investors separate “spend” from “revenue outcomes.”

Goldman highlights dispersion: investors aren’t rewarding all big spenders equally; confidence in revenue outcomes matters.

Partner takeaway: expect more selectivity in who hyperscalers amplify.

Translation: hyperscalers will increasingly prioritize partners who:

drive measurable consumption

have repeatable enterprise wins

show fast time-to-value (and low-friction procurement)

4️⃣ The spotlight is moving from infra to platforms and apps

Goldman sees AI monetization now involve AI platform companies (database + dev tools) and expects the next phases to include AI “productivity beneficiaries,” not just infrastructure.

5️⃣ We’re still early in the buildout cycle

AI capex is at 0.8% of GDP now vs 1.5% peaks in prior tech cycles; Goldman says capex would need to reach $700B in 2026 to match the late-90s telecom peak.

Meaning: more urgency, more building, more programs, more marketplace expansion.

If 2026 is “build mode,” partner leverage is to be the distribution + monetization engine: help hyperscalers to make buying simple, prove consumption impact, and remove friction in marketplace + co-sell. This is when you’ll likely see most support from them.

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value