The market is uneven, and the data is stark so it feels like a major divergence.

I looked at public market performance over the last 12 months (Jan 2025 – Jan 2026), comparing the Hyperscalers against the BVP Nasdaq Emerging Cloud Index.

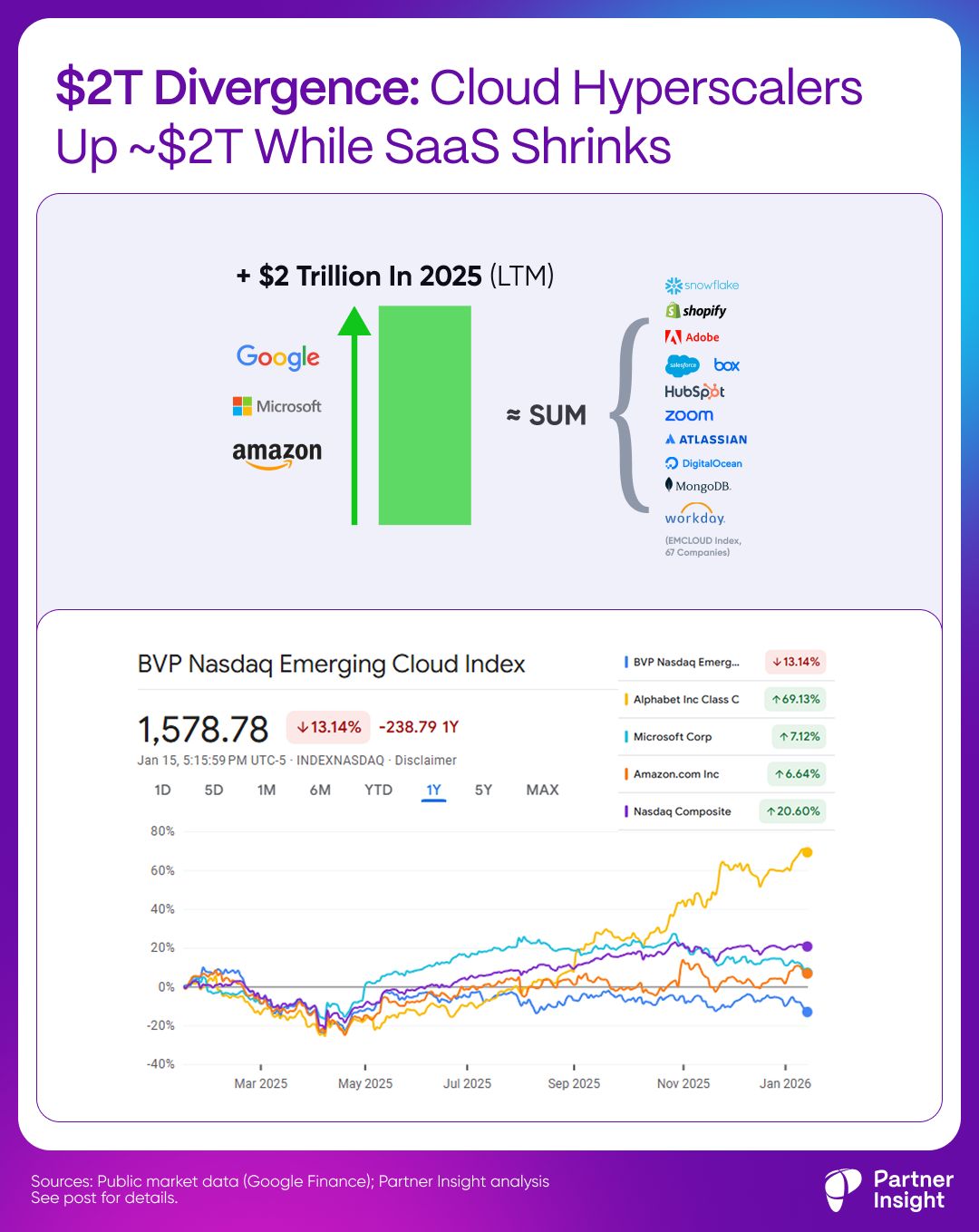

”SaaS Recession” feels real

The BVP Emerging Cloud Index—which tracks a composite of ~75 of the most promising public cloud SaaS companies (see logos) - is down ~13% over the last year.

While the broader Nasdaq rose ~20%, the cloud SaaS basket didn’t just lag; it actually shrank.

At the same time, the hyperscalers moved the other way:

Alphabet Inc. +69%

Microsoft +7%

Amazon +7%

Quick math:

Today, Alphabet + Microsoft + Amazon are worth ~$10T combined.

Based on their 12-month stock moves, they added roughly ~$2T of market value over the last year.

Now compare that with the SaaS cohort: BVP’s index is down ~13%. That’s ~$0.3T erased.

So while the SaaS universe shrunk, hyperscaler platforms grew — massively.

In fact, they added value roughly equal to the entire BVP index, which represents the cloud SaaS universe with ~$2.1T of total market cap.

Not all hyperscalers grew equally. And yes, these are diversified businesses. Same with SaaS companies - some are really winning now. But the directional trend has been now consistent for a couple of years:

Markets are pricing in that AI and cloud are the two growth engines — and the value is accruing around the platforms that control distribution, drive AI adoption and host customer data.

And here’s the part we shouldn’t ignore:

Those same hyperscaler platforms are now reinvesting $300B+ per year into AI infrastructure.

So we’re not just looking at today’s market caps — markets are pricing the future scale of these ecosystems.

This also isn’t just “AI hype.” It’s wallet consolidation.

CIOs and CFOs are under immense pressure to rationalize their stacks. They’re cutting discretionary point solutions and doubling down on platforms where they already have committed cloud spend.

Does it all mean that SaaS is dying? Not quite.

SaaS is changing and realigning to an AI-first world:

Buyers are consolidating spend

Point solutions face more scrutiny

Platforms that control data, distribution, and budgets have more gravity

You need to become AI-first, and it’s actually non-trivial

The top alliance leaders know this.

They grow through hyperscaler marketplaces, attaching to budgets that keeps growing: $531B in cloud commits.

They’re treating cloud alliances and marketplaces as a core GTM motion to accelerate SaaS realignment and tap into AI/cloud boom.

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value