But the shape of the growth is what matters.

I rebuilt the Gartner forecast into a 2025 → 2026 view, and three things stand out for alliance leaders.

1️⃣ Services is the most interesting signal: AI adoption is becoming partner-led at scale

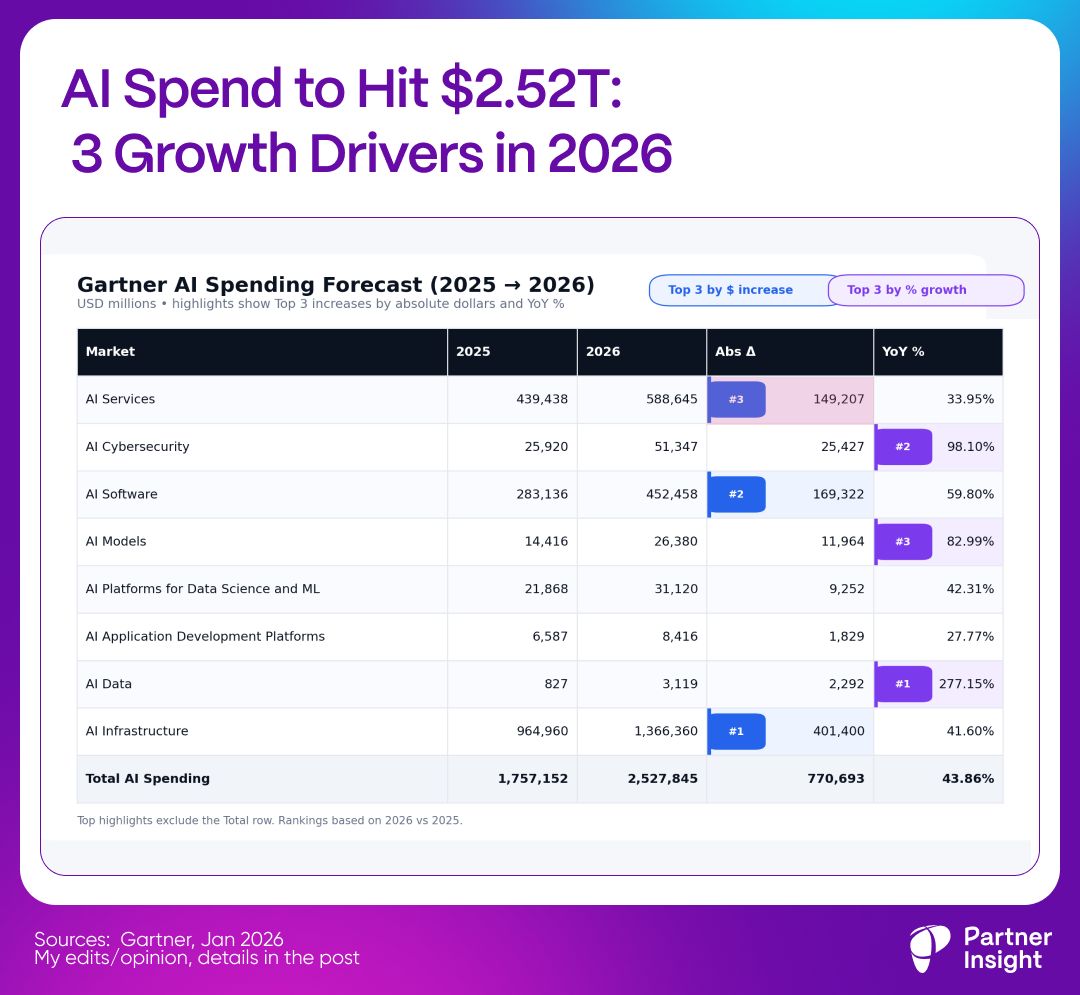

AI Services is the 3 biggest absolute growth bucket — adding $149B in 2026 alone.

That’s Gartner highlighting what most operators already feel:

AI success is less about a “feature launch” and more about implementation — integration, governance, security reviews, data readiness, change management, and ongoing optimization.

This is where partners win.

SIs/MSPs aren’t an add-on. They’re the adoption engine that makes AI usable inside real companies.

If you lead alliances, this should inform your partner strategy: your “AI partner stack” is becoming a repeatable delivery motion.

2️⃣ Gartner’s bigger message on SaaS: incumbents have a winning path — if they prove outcomes

There’s a loud narrative that “SaaS is disrupted by AI.” Gartner pushes back:

“Because AI is in the Trough of Disillusionment throughout 2026, it will most often be sold… by their incumbent software provider…”

In plain language: buyers still prefer familiar vendors — but only when ROI is defensible.

My view: both outcomes will likely happen.

Some legacy software companies will accelerate (distribution, budgets, procurement paths, installed base).

Others will get disrupted (if they can’t ship real outcomes, or AI collapses differentiation).

The key takeaway: the default outcome isn’t “SaaS dies.” It’s “SaaS gets re-ranked by outcomes.”

3️⃣ Infrastructure is the gravity — turning cloud into the distribution layer for everything else

Infra shows the biggest dollar increase. Gartner calls out providers “building out AI foundations,” with infrastructure adding $401B in 2026.

When infrastructure becomes the largest and fast-expanding pool, the cloud becomes the distribution layer for everything else — software procurement, services delivery, and the operating model around it.

If you’re not aligned to hyperscaler motions, you’re not aligned with the strongest pull.

Fastest % growth (small bases, loud signals):

AI Data grows ~3x (data readiness is key)

AI Cybersecurity nearly doubles (governance and risk budgets are catching up fast)

AI Models also grow quickly, though from a smaller base than infra/software/services.

What this means for marketplaces

Put those signals together and the implication is clear. If the fastest-growing spend pools are infrastructure + software + services, the winners will be the companies that can:

attach to hyperscaler infrastructure budgets (cloud consumption, committed spend, procurement convenience),

sell AI software as an expansion of existing buying paths (like marketplaces)

and package services so adoption doesn’t stall after purchase

PS. Source

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value