Let’s look at the tech service market, where partnerships are now crucial and compression and expansion happen at the same time.

McKinsey & Company frames the shift as we move from creating code to agentic AI—software that can take actions across systems.

Rules for service providers, SIs, ISVs and hyperscalers are changing.

⬇️ Where the market is compressing

A lot of work that used to justify headcount or long service engagements is getting cheaper:

routine execution is increasingly automated

more teams are building capability in-house

repeatable delivery is harder to price by the hour

Pure-play AI startups and platform providers will sometimes go direct, bypassing parts of the traditional SI motion.

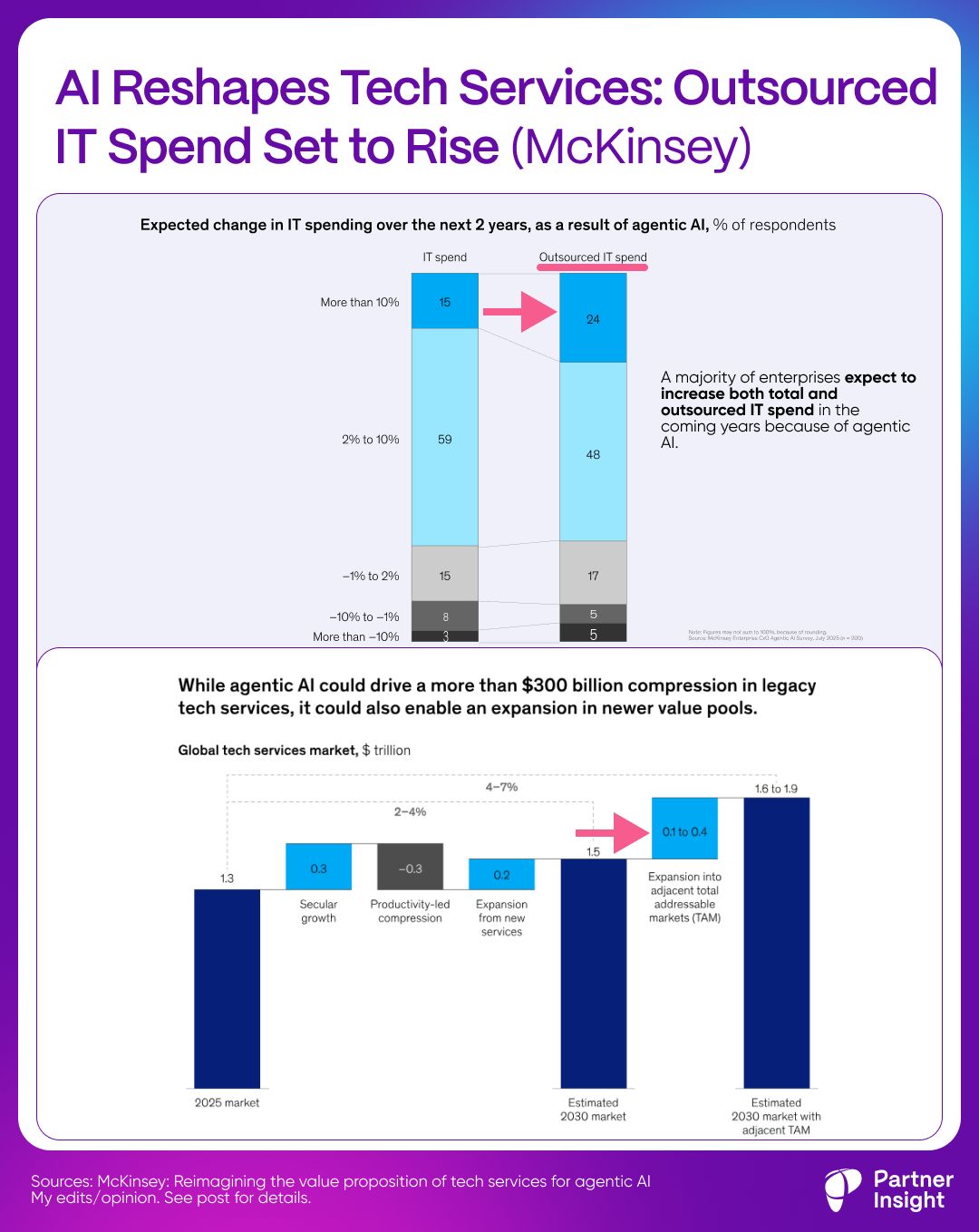

McKinsey estimates this could contract parts of traditional Tech Services by 20–30%. Services aren’t dying — but services tied to manual execution face the most pressure.

⬆️ Where the market is expanding

At the same time, scaling agents creates new spend. McKinsey estimates $100B–$400B of incremental opportunity by 2030, including:

Workflow services ($200B): designing the architecture, governance, and security for agents. Making agents work in the enterprise requires complex integrations, permissions, monitoring, and exception handling—problems most teams can’t solve alone.

Business function transformation: redesigning how departments (HR, support, ops) run with “human + agent” workflows.

Partnerships and ecosystems matter more than ever

Historically, companies scaled first, then partnered. In the agentic era, many will need to partner before scale to offer a complete solution.

No single vendor delivers end-to-end agentic AI. Real deployments demand a best-of-breed mesh across models, orchestration layers, SaaS platforms, data, and security. In practice, the fastest path to production is usually an ecosystem play—not a single-vendor promise.

That shifts market dynamics:

Service providers increasingly productize delivery (“service-as-software”) by building reusable IP, not just selling hours.

Marketplaces matter more as packaging and procurement rails for repeatable solutions—especially when integrations and controls are proven.

Hyperscalers are foundational, but partnerships become less about resale mechanics and more about deep technical integration and shared delivery patterns.

What winners tend to do

Winners won’t be the broad generalists. They’ll be specialized builders who:

bring real domain expertise (you can’t build a healthcare claims agent without claims expertise)

align pricing to outcomes

treat ecosystem readiness as a first-class product requirement, not a late-stage GTM add-on

The market is adjusting for those who sell effort. It’s expanding for those who can reliably deliver outcomes.

PS. Source

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value