This unprecedented wealth creation reveals a deepening divide in tech that's reshaping how software is built, bought, and sold.

Let's look at the numbers (2024 YTD):

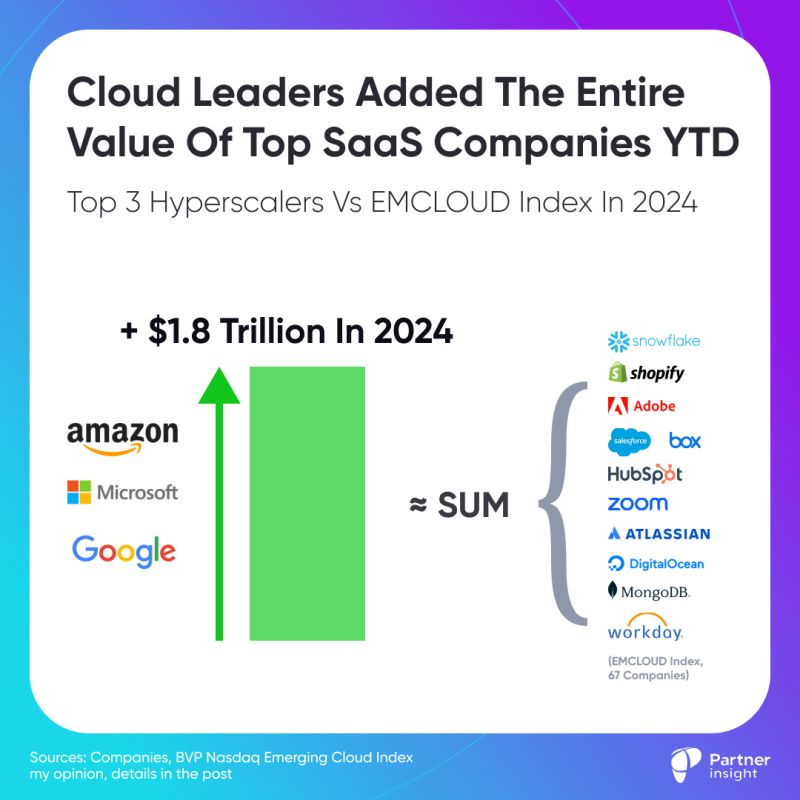

The Big Three added $1.8T combined, showing combined market cap growth of 29%.

Amazon

Market cap: $2.32T

Growth: 49%

Added YTD: $748B

Market cap: $2.32T

Growth: 36%

Added: $560B

Microsoft

Market cap: $3.25T

Growth: 18%

Added: $457B

While hyperscalers soared, the BVP Emerging Cloud Index (EMCLOUD) - tracking top SaaS companies - grew just 14.3%. The contrast is stark but unsurprising.

As a reminder BVP Nasdaq Emerging Cloud Index (EMCLOUD) is calculated and maintained by Nasdaq and sponsored by Bessemer Venture Partners. It includes the weighted average of 67 top SaaS companies with >500M in market cap.

Among them are such iconic names in software as:

Adobe, Atlassian, Box, Cloudflare, Confluent, CrowdStrike, DigitalOcean, HubSpot, MongoDB, PayPal, Salesforce, ServiceNow, Shopify, Snowflake, Workday, Zoom, and Zscaler.

What's driving this divergence?

Hyperscalers are uniquely positioned to capture value from the AI revolution through:

Massive compute infrastructure powering AI workloads

Deep partner ecosystems accelerating AI adoption

Cloud marketplaces becoming the dominant distribution channel for software

This creates a powerful flywheel: As hyperscalers grow stronger, more software companies align their GTM with cloud marketplaces, further cementing hyperscalers' position.

To prove the point, two other tech giants riding the cloud and AI wave registered even more dramatic gains (all data as of Dec 19):

NVIDIA

Market cap: $3.2T

Growth: 162%

Added YTD: $1.97T

NVIDIA single-handedly added more value than all three hyperscalers combined

Oracle

Market cap: $472B

Growth: 63%

Added: $182B

Oracle showed highest growth among clouds after doubling down on cloud strategy and partnering with other hyperscalers. It's about to enter $500B club.

🕹️ Hyperscalers aren't just benefiting from the AI boom - they're orchestrating it

Their cloud marketplaces have become the key distribution channel for software, while their AI platforms and partners are becoming the foundation for next-gen applications.

The question for 2025: Will this concentration of power accelerate even further as AI moves from experimentation to widespread enterprise deployment?

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value