The platform now sits at the center of cloud storage, distributed production, and enterprise file workflows, where customers often need software, services, marketplace procurement, and technology partners to come together.The shift took 13 months and a full rebuild of how LucidLink sells with partners.

"You never want a customer to tell you 'I want to buy through this partner, or I want to buy through this marketplace,' and you have to say no."

That line from David Mauer, VP of Global Partner Ecosystem at LucidLink, explains the logic behind the company's partner program relaunch. If a customer asks to buy through a reseller, MSP, AWS Marketplace, or an SI, the answer should be yes.

The setup

David Mauer joined LucidLink as VP of Channel and Alliances a year ago. He inherited a channel program that wasn't pulling its weight.

In FY25, as the rebuild took hold, channel generated nearly $5M in net new ARR — more than one-third of net new ARR. Reseller headcount grew more than 30% YoY.

The FY26 plan is more ambitious. It targets a 45% channel mix of net new ARR, a 5x expansion of AMER partner activity, and a 60% partner-touched share of total deals.

How do they do it, given that LucidLink builds workflow software for creative teams in media, entertainment, and sports?

Turns out partner-first GTM architecture is critical in vertical workflow markets where buyers need software, services, cloud marketplace procurement, and technology integrations to work together.

Building Partner Architecture

In LucidLink’s original channel model VARs could transact the product, but they hit a ceiling.

Resellers transacted, but couldn't manage at scale. Marketplace was nascent and disconnected from the channel. Technology alliances didn't bundle commercially. Each worked in isolation, overlapping and making it non-scaleable.

As LucidLink moved deeper into enterprise media and entertainment workflows, the customer conversation became more complex. Buyers were no longer asking for a point solution in isolation. They were asking how LucidLink fit into a broader production stack, cloud strategy, media asset management workflow, systems integration plan, and procurement path.

That changed the partner requirement.

The rebuild was designed to clear every buying path the customer might need in a single transaction: reseller-led, AWS Marketplace, AWS co-sell, MSP-managed, technology alliance bundle, or enterprise direct.

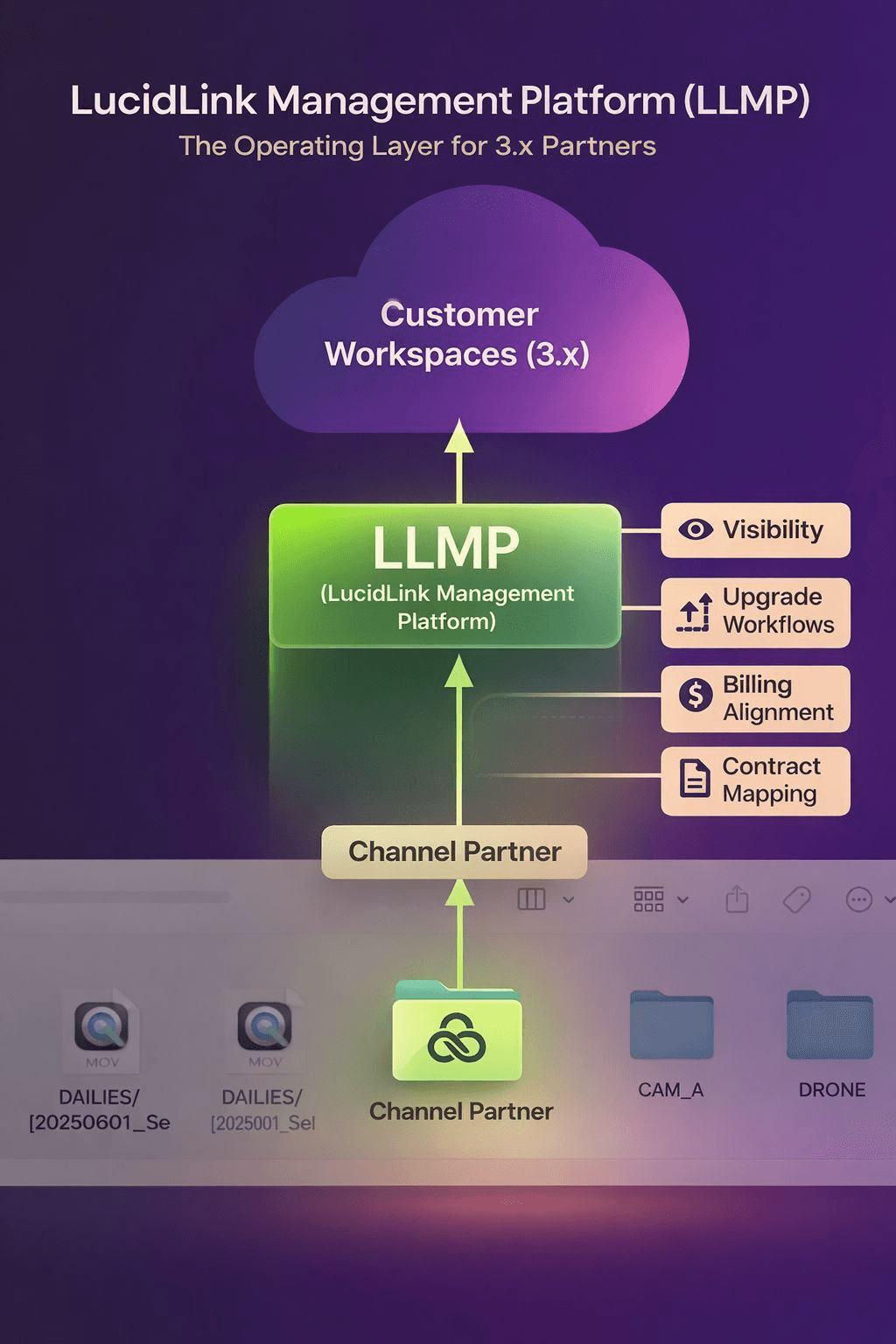

LLMP: partners need operational control to drive revenue

LucidLink launched the LucidLink Management Platform (LLMP) to give partners the infrastructure to provision, manage, and bill LucidLink at scale across their customer base.

"The channel isn't an add-on to our strategy, it's central to it. LLMP is about giving partners real operational leverage and differentiation with their customers." — David Mauer

What makes LLMP unusual is the multi-program design. It extends beyond traditional channel management and supports several partner models in parallel:

Channel resellers and VARs

Managed service providers

Large enterprise customers who manage LucidLink internally at scale, with nested access for the channel partners serving subsets of the business

Holding-company-style marketing groups (Omnicom, WPP) that operate as MSPs over their own sub-agencies

A media agency group, a post-production network, a broadcaster, and a systems integrator may all touch the same customer environment differently. If the partner platform only supports one route, the program creates friction inside the very accounts it is supposed to help expand.

LLMP gives partners a structured view of partner-managed environments — visibility into customer state, contracts, and billing — so they can operate in confidence without escalating back to LucidLink.

Cloud Marketplaces as the commercial backbone

LucidLink's marketplace strategy sits inside the same architecture.

AWS is the anchor hyperscaler relationship today, with active marketplace and co-sell motion. Google Cloud and Oracle Cloud Infrastructure are part of the next phase of expansion.

The marketplace is not a separate transaction desk that sits next to channel. Mauer's team is building the partner program so marketplace, co-sell, channel, and technology alliances attach to the same customer motion. That is how leading cloud GTM programs are evolving.

"You have to make deals as frictionless as possible. Customers are going to marketplaces for either cloud spend, or budget reasons, or just because it's that frictionless model. Channel partners are also involved. You have to meet where your customers and your channel partners are." — David Mauer

A customer may want to use AWS Marketplace because budget already sits in a cloud commitment. A reseller may still own the relationship. A technology alliance partner may shape the solution. A systems integrator may be needed to implement the workflow. AWS may influence the deal through co-sell or one of its programs.

The commercial route and the partner route are merging.

For LucidLink, that is especially relevant because its product sits in the middle of large file collaboration, cloud storage, media workflows, distributed teams, and production operations. The buyer is solving a workflow problem, then trying to buy it through the least painful route. The customer should not have to reorganize the buying process around the vendor's internal GTM chart.

That is why LucidLink is, in Mauer's words, "striving to be a partner ecosystem-led company."

Channel partners surface and develop the deal. LLMP enables the practice underneath. Marketplace transacts inside the customer's existing cloud commitment. Remove any of the three and the model breaks. The integration is the point.

AWS BOX: productized bundle

The practical example of how LucidLink scales its partner architecture is the AWS Business Outcomes Xcelerator program (BOX), where LucidLink has joined forces with iconik and Embrace.

Multiple ISVs and regional channel partners align around a customer outcome rather than show up as separate vendor pitches.

LucidLink provides the high-performance file access layer. iconik brings media asset management. Embrace adds workflow automation and orchestration. AWS provides cloud infrastructure, marketplace, co-sell context, and partner program gravity. Regional channel partners become the field motion.

That combination is close to how customers describe the problem and how they want to buy — from one hand. The result is a more complete ecosystem package.

"Ecosystem innovation is transformative. The bundle changes the math on a lot of deals." — David Mauer

AWS BOX gives LucidLink a way to test the model with various partner combinations. Additional BOX-style workflows are already in development.

The early signal from the field has been strong:

At NAB 2026, six new ITAP (Integrated Technology Alliance Partner) candidates were identified, representing more than $3M in partner-influenced pipeline across 32 opportunities from a single trade show week.

The buying pattern underneath is simple. Customers want business outcomes. Hyperscalers want consumption and marketplace growth. ISVs need partners to assemble the full solution.

LucidLink and AWS BOX show where marketplace-led GTM is be heading: packaging multi-vendor outcomes so the buyer can procure a complete workflow through the commercial path they already prefer.

What 2026 looks like

LucidLink's partner program is already approaching $1M in net new ARR in 2026. The targets above it — 45% channel mix, 60% partner-touched deals, 5x AMER expansion — are the operating measure of whether the architecture holds.

The harder question is what LucidLink's trajectory implies for the broader market.

Most ISVs treat partner programs as a layer added on top of direct sales. LucidLink rebuilt the company GTM around the assumption that the customer's buying path is the architecture, and direct sales is one route inside it.

If a media collaboration vendor can run that play to 39% of revenue, the next conversation is not whether the partner model works. It's which category it lands in next.

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value